ⓘ Written and reviewed per our independent editorial methodology.

The honest answer is that Chime makes money mainly from interchange, the small fee Visa charges a merchant every time you swipe your Chime card, not from monthly or overdraft fees. A regulatory carve-out lets its partner banks charge a higher swipe fee, and that is what funds the “free” account.

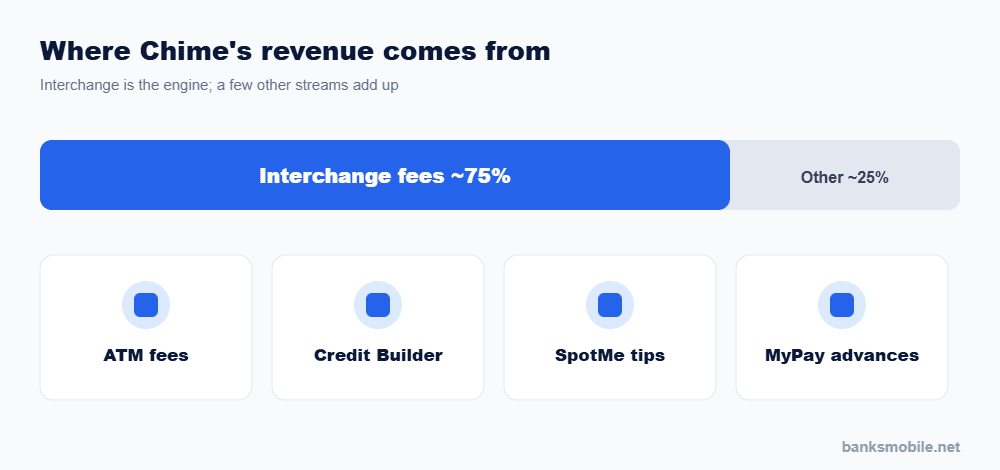

- Chime earns roughly 75 cents of every revenue dollar from card interchange.

- The Durbin Amendment exempts small partner banks from interchange caps, so they can charge merchants more.

- Secondary income: out-of-network ATM fees, the Credit Builder card, SpotMe tips, and MyPay earned-wage access.

- For 2026 Chime guided to about $2.6 billion in revenue and its first full profitable year.

“Free banking” makes people suspicious, and they are half right to be. If an app hands you a checking account with no monthly fee, no overdraft fee, and no minimum balance, the natural question is who is paying for it. So how does Chime make money? The distinction that matters is this: Chime does not sell your data, and it does not charge you the fees a legacy bank does. It gets paid by merchants, quietly, every time you swipe.

Chime is one of the largest online banking apps in the US, and for 2026 it guided to roughly $2.6 billion in revenue. Below I break down exactly where that money comes from, why a regulatory quirk makes the model work, and what it means for you as a member. If you are weighing Chime against another app, it also helps to read how a fintech differs from a bank first.

The short answer: how does Chime make money?

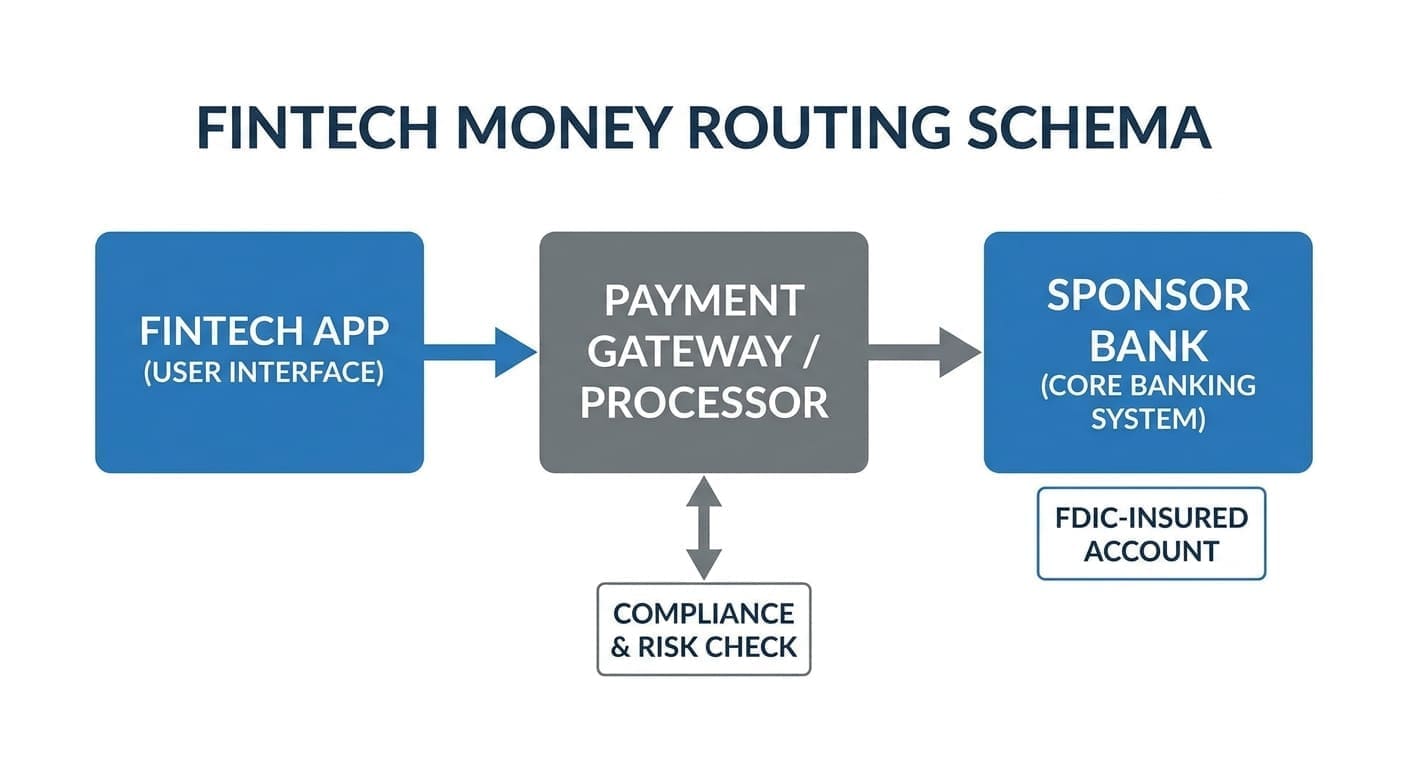

Chime runs a “free-for-you, paid-by-merchants” model. Its largest revenue source by far is interchange: the fee that card networks like Visa charge a store each time a customer pays by card. Because Chime issues millions of cards and members use them constantly, those small per-swipe fees compound into the majority of the company's income. Everything else, ATM fees, the SpotMe tip jar, lending-style products, sits on top of that foundation.

Interchange fees: the real engine

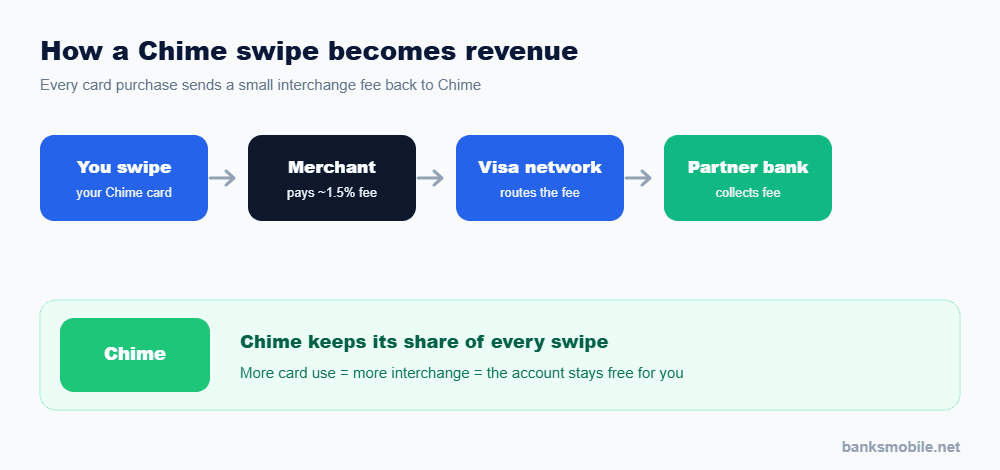

Interchange is roughly 1.5% of each purchase on a Chime card, and Chime reportedly keeps about 75 cents of every revenue dollar from it. That is why the app nudges you to use the card more: early direct deposit, round-ups, and fee-free overdraft all exist to increase swipes. Here is the flow, step by step:

This is standard across the card industry, what makes Chime interesting is how much more interchange it can collect than a big bank, thanks to a 2010 rule. You can read the mechanics straight from the Federal Reserve's Regulation II overview.

The Durbin Amendment advantage

Here is the part most explainers skip. The Durbin Amendment caps debit interchange for large banks but exempts smaller ones. Chime is not a bank; it partners with banks that sit under the $10 billion asset threshold, so they can charge merchants far more per swipe than a giant like Chase is allowed to. Chime shares in that richer fee. To see who actually holds your money, read what bank Chime uses.

Banks with $10B+ in assets (Chase, Bank of America) are capped by the Durbin Amendment at roughly 0.05% + 21 cents per debit swipe.

Its partners sit under $10B, so they are exempt and can charge merchants around 1.5%. That gap is the whole business model.

That gap is not a loophole so much as the intended effect of the law, which aimed to help smaller institutions compete. For the official framing, see the Federal Reserve's Durbin rule announcement. It is also why so many digital banks differ from traditional banks on fees: their economics start from a different place.

Chime's other revenue streams

Interchange is the engine, but a handful of other streams add up, and they are growing as Chime expands beyond a simple checking account:

| Revenue stream | How it works | Roughly how big |

|---|---|---|

| Interchange fees | Visa’s ~1.5% merchant fee on every swipe | Majority (~75%) |

| Out-of-network ATM fees | Charged at non-partner ATMs | Small |

| Credit Builder card | Interchange on the secured card’s spending | Growing |

| SpotMe tips | Optional tips after a fee-free overdraft | Small |

| MyPay (earned wage access) | Optional instant-transfer fees on pay advances | Scaling fast |

MyPay, Chime's earned-wage-access product, scaled to more than $400 million in annualized revenue, a sign the company is diversifying. Its money-movement features and peer-to-peer options keep members inside the ecosystem, which in turn keeps the card in their wallet. If you want the corporate numbers, Chime publishes them through its investor relations page.

To put the scale in perspective, Chime serves millions of members and processes billions of dollars in card spending every year. At roughly 1.5% interchange, even a modest few hundred dollars of monthly swipes per active member adds up to the bulk of that $2.6 billion revenue guide. It is a volume business: thin margins on each transaction, but an enormous number of transactions. That is also why growth in active members and card usage, rather than new fees, is the metric investors watch most closely, and why keeping the account free is a feature, not a sacrifice.

So is Chime really free?

For everyday use, yes. The honest answer is that there are no monthly, overdraft, or minimum-balance fees, but “free” has edges worth knowing. Here is the clean split:

- No monthly maintenance fee

- No overdraft fee (SpotMe up to a limit)

- No minimum-balance fee

- In-network ATM withdrawals

- Out-of-network ATM fees

- Optional instant-transfer fees

- A voluntary SpotMe tip

You are not the product. Your spending is. That single fact explains almost everything about how Chime is built.

So the trade is straightforward: you get genuinely fee-free everyday banking, and Chime gets a cut of your spending plus optional revenue from features you choose to use. If your goal is to keep more of your money, pair a free account like this with a high-yield savings account, and use our free savings calculator to see how a small monthly deposit grows. New to the terms? Start with what APY means and what a high-yield savings account is, then how to choose one.

What Chime's business model means for you

Understanding how Chime makes money is not academic, it changes how you should use the account. Because Chime earns when you swipe, its incentives line up with yours on fees: it genuinely wants the everyday account to stay free so you keep reaching for the card. Where your interests diverge is on savings. Interchange rewards spending, not balances, so Chime has little reason to pay you a market-leading yield. That is why the smart play is simple, spend from Chime, and keep your savings somewhere that actually pays you.

The model also explains the product roadmap. Every feature Chime ships, early direct deposit, SpotMe, the Credit Builder card, MyPay, exists to deepen the relationship and lift card activity or add a new, optional fee stream. None of it requires charging you a maintenance fee, which is exactly the point. For the full picture of the company behind the app, our Chime Bank review walks through the accounts, limits, and where it falls short, while Chime vs Cash App shows how a direct rival monetizes differently, and Chime vs SoFi contrasts a spending-first app with a yield-first one.

The regulatory backdrop matters too. If lawmakers ever extended interchange caps to smaller banks, the economics that keep Chime free could tighten overnight. For now the model is durable, and Chime guided to its first full year of GAAP profitability in 2026. If you care how these fee rules evolve, the Consumer Financial Protection Bureau is the agency that polices overdraft and junk-fee practices, and its rulings shape what every app-based bank can and cannot charge.

Frequently asked questions

Does Chime charge hidden fees?

No monthly, overdraft, or minimum-balance fees. You can still pay out-of-network ATM fees or optional instant-transfer fees, and SpotMe invites a voluntary tip.

How does Chime make money if it is free?

Mainly through interchange, the fee Visa charges merchants each time you swipe. Chime and its partner bank share it, so the account stays free for you.

Is Chime a real bank?

Chime is a fintech, not a bank. Banking and FDIC insurance come from partner banks. See which bank Chime uses and whether Chime is safe.

Will Chime start charging fees now that it is public?

Its whole pitch is fee-free banking, so a monthly fee is unlikely. Expect it to lean on interchange and newer products like MyPay instead.

The principle to remember: a “free” bank is never free to run, so always find the revenue source before you trust the product. With Chime, that source is your card, transparent, and aligned with keeping fees off your statement. Bank there happily; just keep your savings in a higher-yield account, because interchange pays Chime, not you. Ryan Cooper