ⓘ Written and reviewed per our independent editorial methodology.

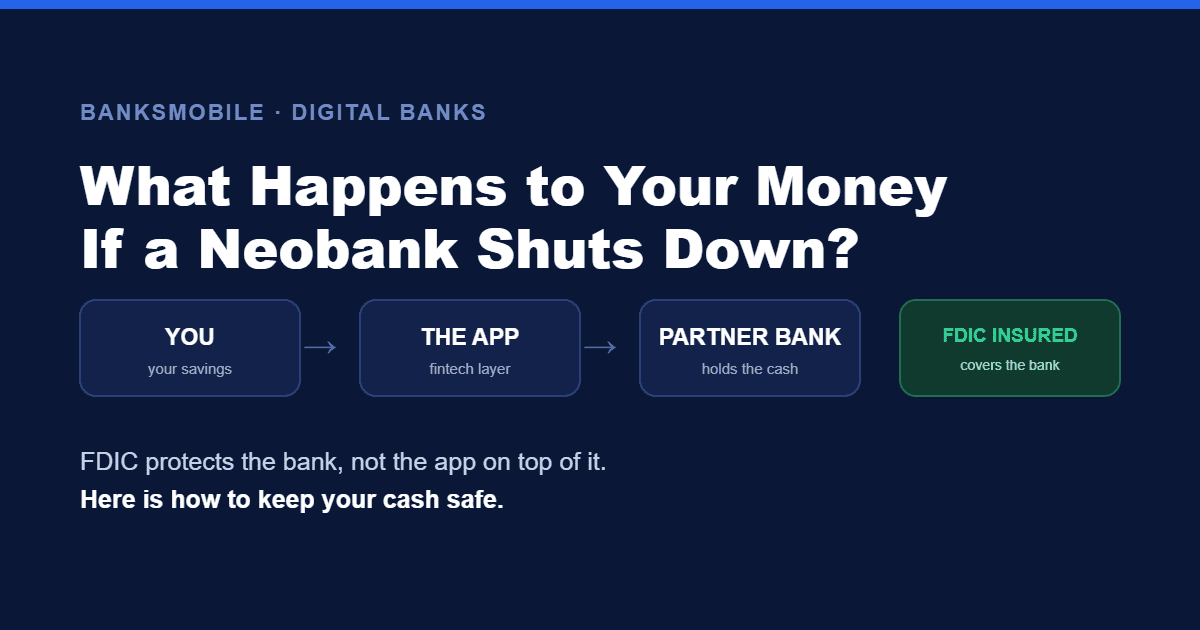

Neobanks have made banking faster, cheaper and friendlier, but they have also quietly changed who actually holds your money. When a slick app sits on top of a bank you have never heard of, one fair question follows: if a neobank shuts down overnight, what happens to your cash?

The honest answer is that FDIC insurance protects you from a bank failing, not from a fintech or its behind-the-scenes plumbing failing. That sounds academic until it is your paycheck that is frozen, and in 2024 it stopped being academic for tens of thousands of Americans.

- If a neobank shuts down because its partner bank fails, FDIC protects you; if the app or its middleware fails instead, it may not.

- In the 2024 Synapse collapse, roughly $265 million in customer funds was frozen across several apps.

- Money in pooled “For Benefit Of” (FBO) accounts is only quickly insurable if records prove exactly who owns each dollar.

- Neobanks with their own charter (Varo) or a clearly named single partner bank remove a layer of risk.

- Verify the partner bank on FDIC.gov, keep your own statements, and spread large balances.

Table of Contents

The Short Answer

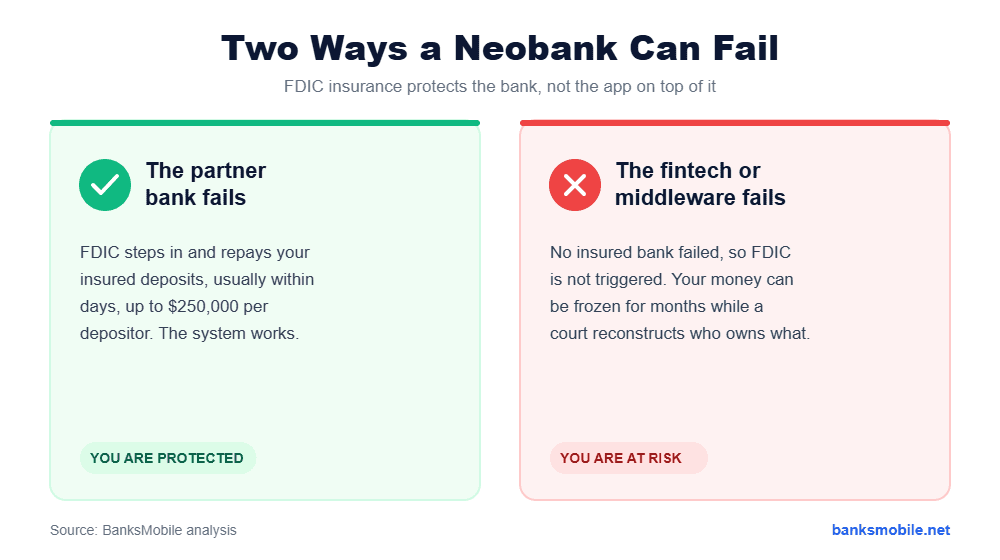

If the bank that actually holds your deposits fails, FDIC insurance reimburses your eligible balances up to $250,000 per depositor, usually within days. That is the system working as designed, and it is genuinely reliable.

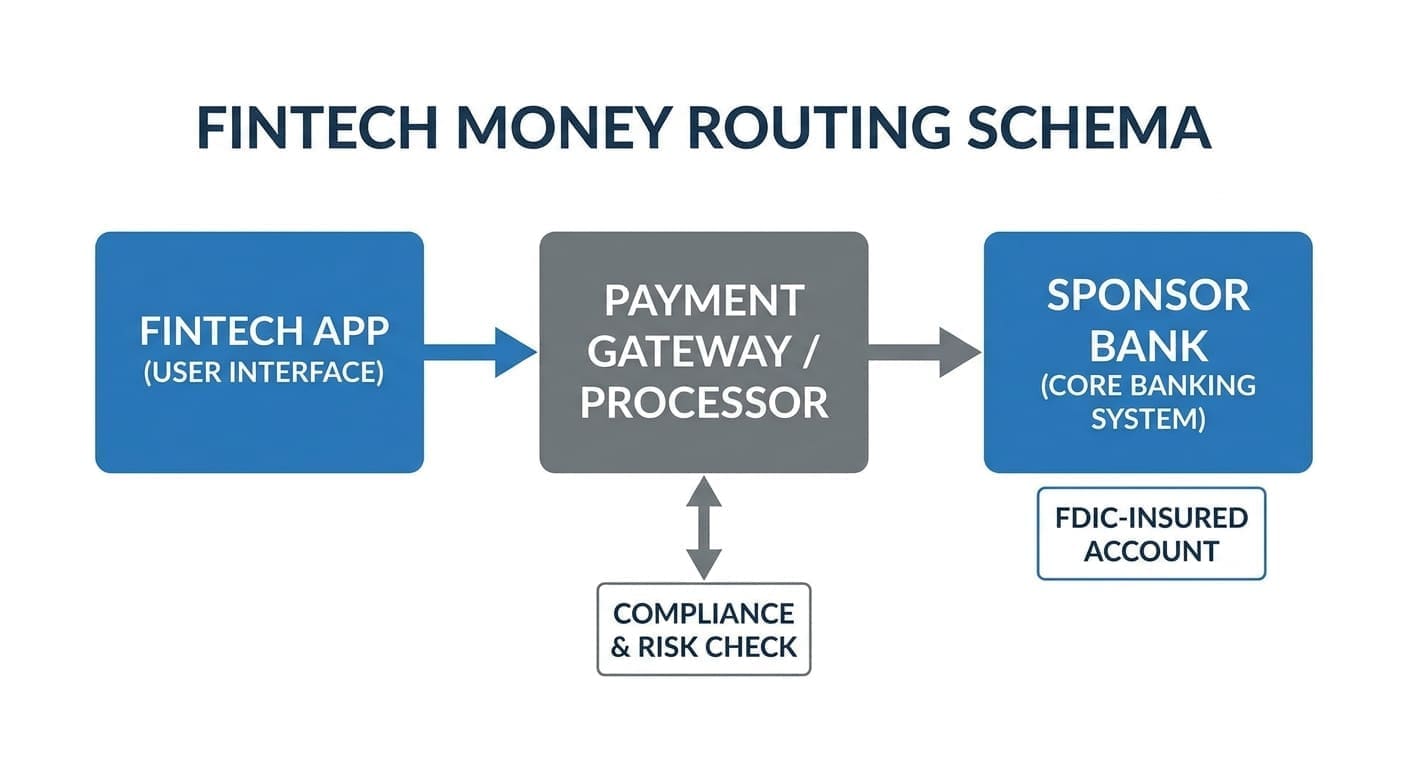

The problem is that most neobanks are not banks. They are technology companies that route your money to a partner bank, sometimes through a third intermediary. FDIC insurance was built for the first scenario, not the second. When the app or the middleware in the middle fails, the insurance does not automatically rescue you, because no insured bank has actually failed.

What FDIC Insurance Actually Covers

FDIC insurance is a federal guarantee that, if an insured bank collapses, depositors are made whole up to $250,000 per depositor, per ownership category. It has an excellent track record, and no one has ever lost an insured deposit because of a bank failure.

When a neobank advertises that your funds are “FDIC insured,” it usually means a partner bank holds the money. Chime, for example, works with The Bancorp Bank, N.A. and Stride Bank, N.A.; see our deep dive on what bank Chime uses and our is Chime safe review. That coverage is real, but it carries one condition: the records have to clearly show the money is yours.

Two Ways a Neobank Can Fail

It helps to picture the two very different failure paths, because your outcome depends entirely on which one happens.

The Synapse Collapse: A Real Cautionary Tale

This is not theoretical. In April 2024, a middleware company called Synapse, which connected dozens of fintech apps to partner banks, filed for bankruptcy. Synapse kept the ledgers that tracked which customer owned which slice of money pooled inside the banks. When it shut down a critical system, roughly $265 million in end-user funds was frozen.

The most painful example was the savings app Yotta, which reached customers through Evolve Bank & Trust with Synapse as the middleman. When the ledgers were examined, large amounts simply did not reconcile. Reporting indicated that Yotta customers who deposited about $64.9 million were offered a combined $11.8 million. Real people watched their savings vanish into a bankruptcy dispute, even though no bank had failed.

No bank failed in the Synapse collapse, yet thousands of people still could not reach their money. That gap is the whole point.

Why “FDIC-Insured” Can Still Leave You Exposed

The mechanism behind the gap is something called a “For Benefit Of,” or FBO, account. Instead of opening an individual account in your name, many fintechs pool all customer money into one big omnibus account at the partner bank, and keep their own internal ledger of who owns what.

FDIC pass-through insurance can still apply to that pooled money, but only if the records clearly and accurately identify each owner. If the company keeping those records fails and the ledger is incomplete, the FDIC cannot quickly tell who is owed what. In response to the Synapse mess, the FDIC moved in late 2024 to require banks to keep better records of fintech customers, precisely so pass-through insurance can actually work. Useful, but it does not erase the risk that exists today.

What Happens Step by Step When a Neobank Shuts Down

When a neobank shuts down, separating the two failure paths makes the likely outcome clear.

| Scenario | Are your insured deposits protected? |

|---|---|

| The partner bank fails, records are accurate | Yes, FDIC pays up to $250,000 per depositor |

| The fintech app itself goes bankrupt | Not directly, FDIC does not insure fintechs |

| The middleware / ledger provider fails (e.g. Synapse) | At risk, if records cannot prove who owns what |

| You authorize a payment to a scammer | No, authorized transfers are not insured or refunded |

How to Protect Your Money

You do not need to abandon neobanks, you just need to use them with your eyes open. A few habits sharply reduce your exposure.

- Verify the partner bank. Find the named bank in the app disclosures and confirm it on the FDIC BankFind tool. No named bank is a red flag.

- Keep your own records. Download monthly statements and screenshot your balance, so you have leverage in any ledger dispute.

- Do not keep everything in one app. Treat an app-only fintech as a spending and saving tool, not the sole home of your emergency fund.

- Spread larger balances across a chartered neobank or a traditional bank, so one broken layer cannot freeze all your cash.

Need a second home for cash? Our guide to high-yield savings accounts can help you choose.

Chartered Banks vs Partner-Bank Apps

One of the cleanest ways to lower this risk is to choose a neobank that holds its own bank charter, because it removes the middleware layer entirely.

Holds its own bank charter (for example Varo) or runs as a bank itself (SoFi Bank, N.A.). No separate middleware ledger sits between you and an insured bank.

A fintech routes your money to one or more partner banks, sometimes through a third-party ledger. Often well run, but more layers means more places a record can break.

Varo won a national bank charter in 2020, and SoFi operates as SoFi Bank, N.A.; see our SoFi review. Partner-bank apps are not automatically unsafe, and many are well run. The difference is simply the number of moving parts. For the bigger picture, read fintech vs digital banking and our ultimate guide to digital banking.

Final Verdict

Compare your options in our digital banks hub.