Written and reviewed per our independent editorial methodology.

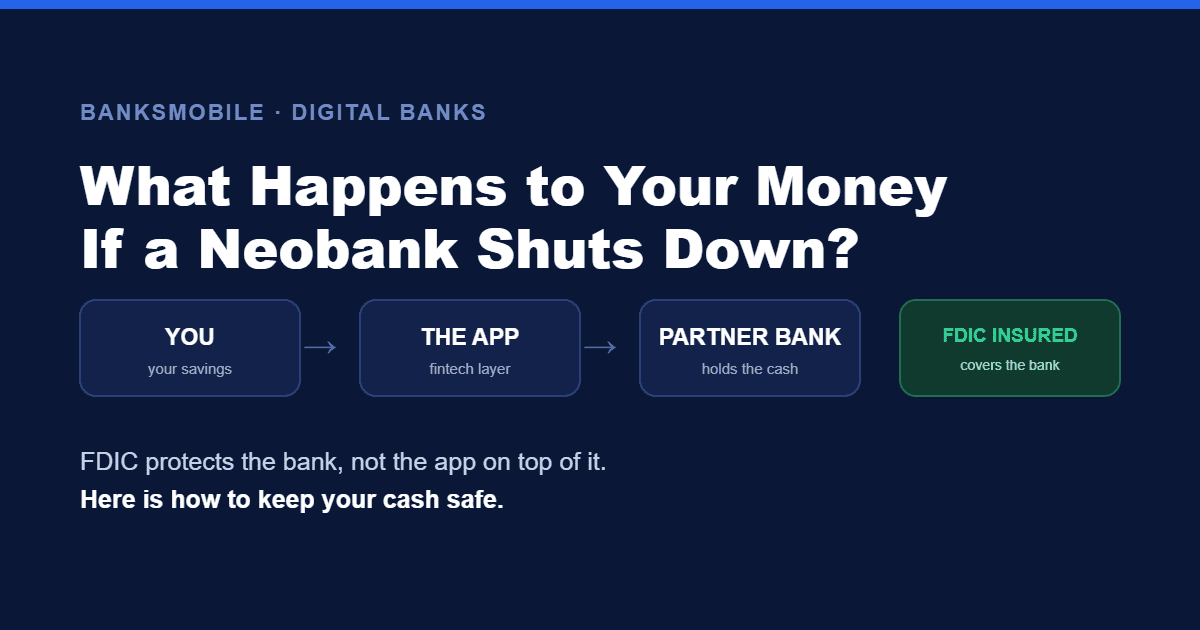

Neobanks are not inherently safe because they are fintech companies, not chartered banks with direct FDIC insurance. Their safety depends entirely on their legal partnership with an FDIC-insured sponsor bank and transparent pass-through coverage structures.

Many people love the convenience and speed of mobile financial apps. However, asking are neobanks safe is the smartest financial move you can make today. The landscape of digital finance has shifted dramatically following recent regulatory crackdowns.

These platforms offer sleek interfaces and competitive yields that attract millions of users. But beneath the hood, they operate very differently from traditional brick-and-mortar institutions. They are technology companies, not actual chartered banks.

Understanding where your money physically sits is absolutely crucial for your financial well-being. We will break down exactly how pass-through insurance works and what happens if a fintech company fails. Your financial security depends on knowing these hidden details.

- ✓Neobanks are fintech companies and do not possess direct FDIC insurance.

- ✓Pass-through FDIC insurance only works if the legal partnership with the sponsor bank is flawless.

- ✓Crypto assets held in digital banking apps are never protected by federal insurance.

- ✓The 2024 Synapse collapse proved that fintech middleware failures can freeze customer funds for months.

Why Are People Questioning Fintech Banking Safety Today?

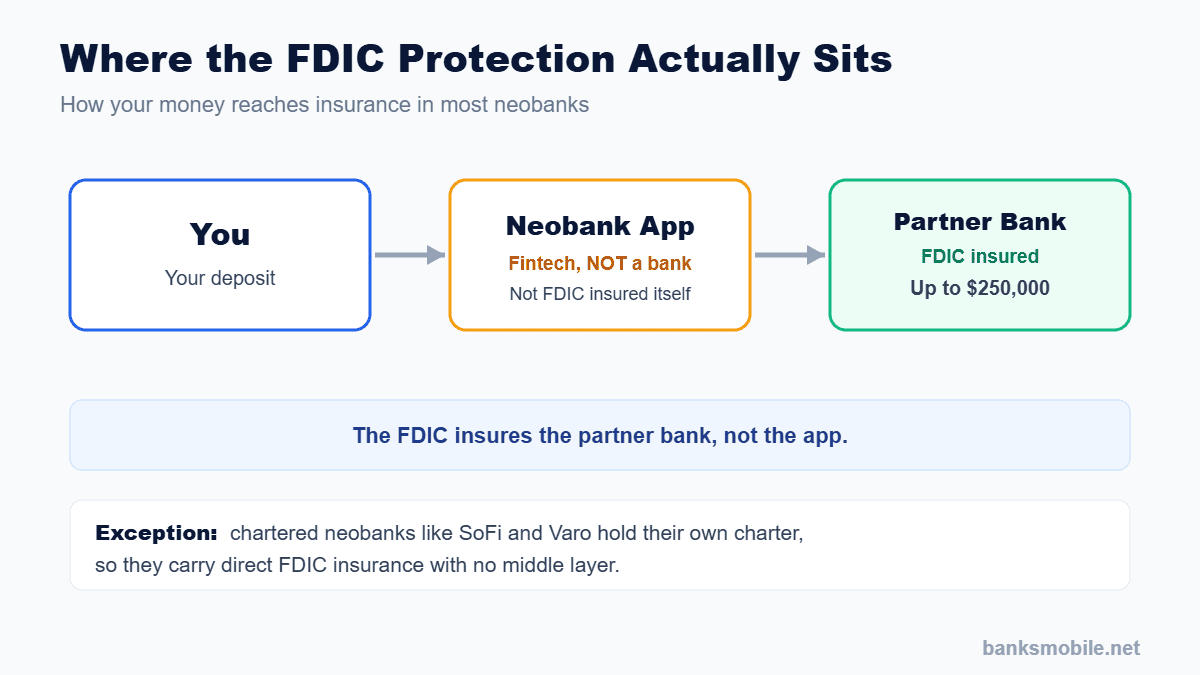

Here is the deal: Neobanks are fintech firms, not chartered banks. They do not hold direct insurance from the Federal Deposit Insurance Corporation.

Instead, they rely on complex partnerships with underlying sponsor banks. This means your money takes a detour before it reaches a secure, regulated vault.

Regulators like the OCC and the Federal Reserve have noticed the cracks in this system. They issued strict joint statements warning banks to increase oversight of their fintech partners.

Sponsor banks now face intense audits regarding their compliance with anti-money laundering laws. If a sponsor bank fails an audit, the fintech app can lose its banking services overnight.

Many consumers learned this the hard way when their accounts were abruptly frozen. You must look past the sleek marketing and verify the actual legal structure of your account.

The banking-as-a-service model grew too fast for regulators to keep up. Now, federal agencies are stepping in to clean up the mess and protect consumers.

This regulatory crackdown is exactly why you need to understand where your deposits live. Trusting a shiny app interface is no longer enough to guarantee financial security.

Always check the fine print at the bottom of a neobank website. If you cannot find the exact phrase indicating deposits are held at a specific Member FDIC bank, your money might be at risk.

How Does Pass-Through FDIC Insurance Actually Work?

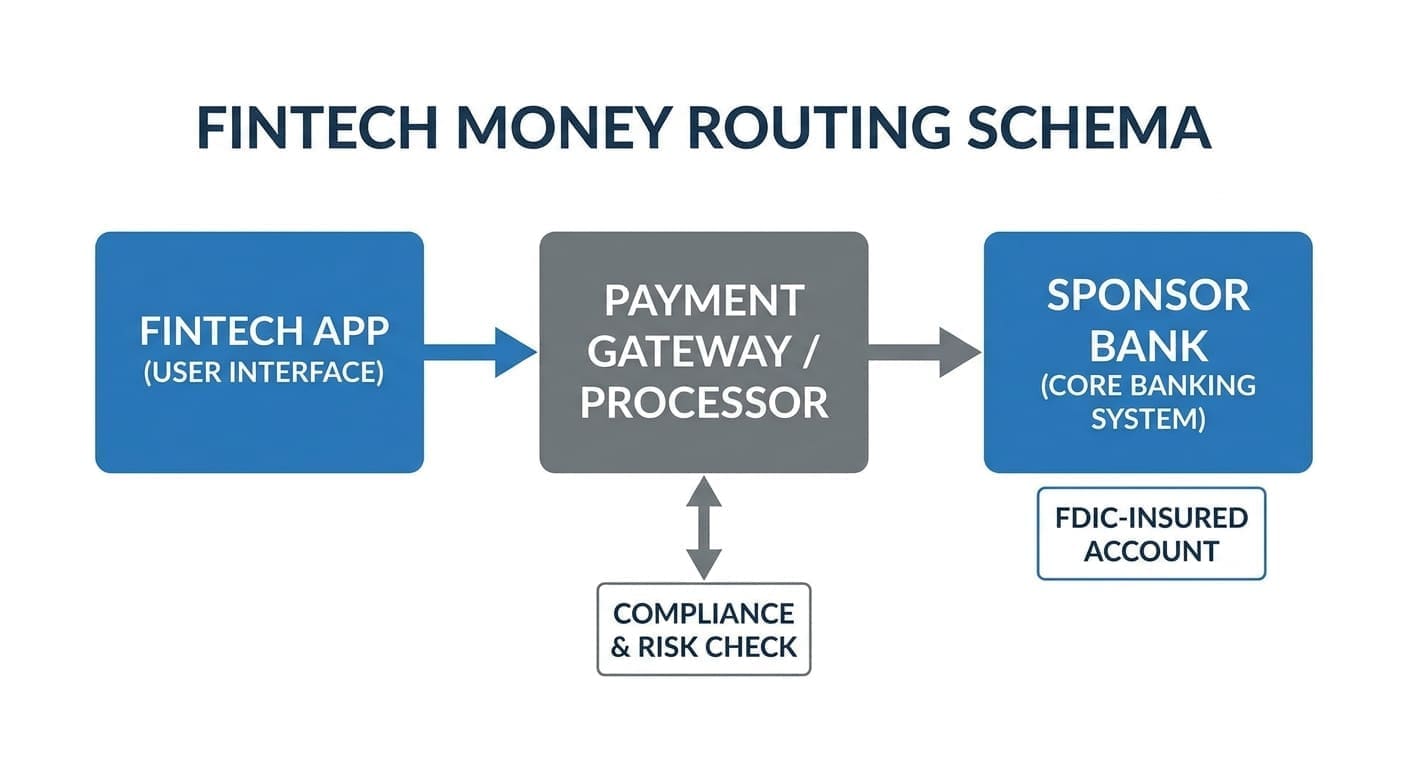

Pass-through insurance is a legal mechanism designed to protect your deposits. It allows a non-bank company to extend FDIC coverage to its users.

However, this protection is entirely conditional. The fintech must establish a flawless principal-agent relationship with the partner bank.

If the legal paperwork is messy, the FDIC will not honor the claim. This is a massive risk that most users never consider when opening an account.

When working properly, your funds sweep into a pooled account at the sponsor bank. The bank keeps a ledger matching your specific balance to the pooled funds.

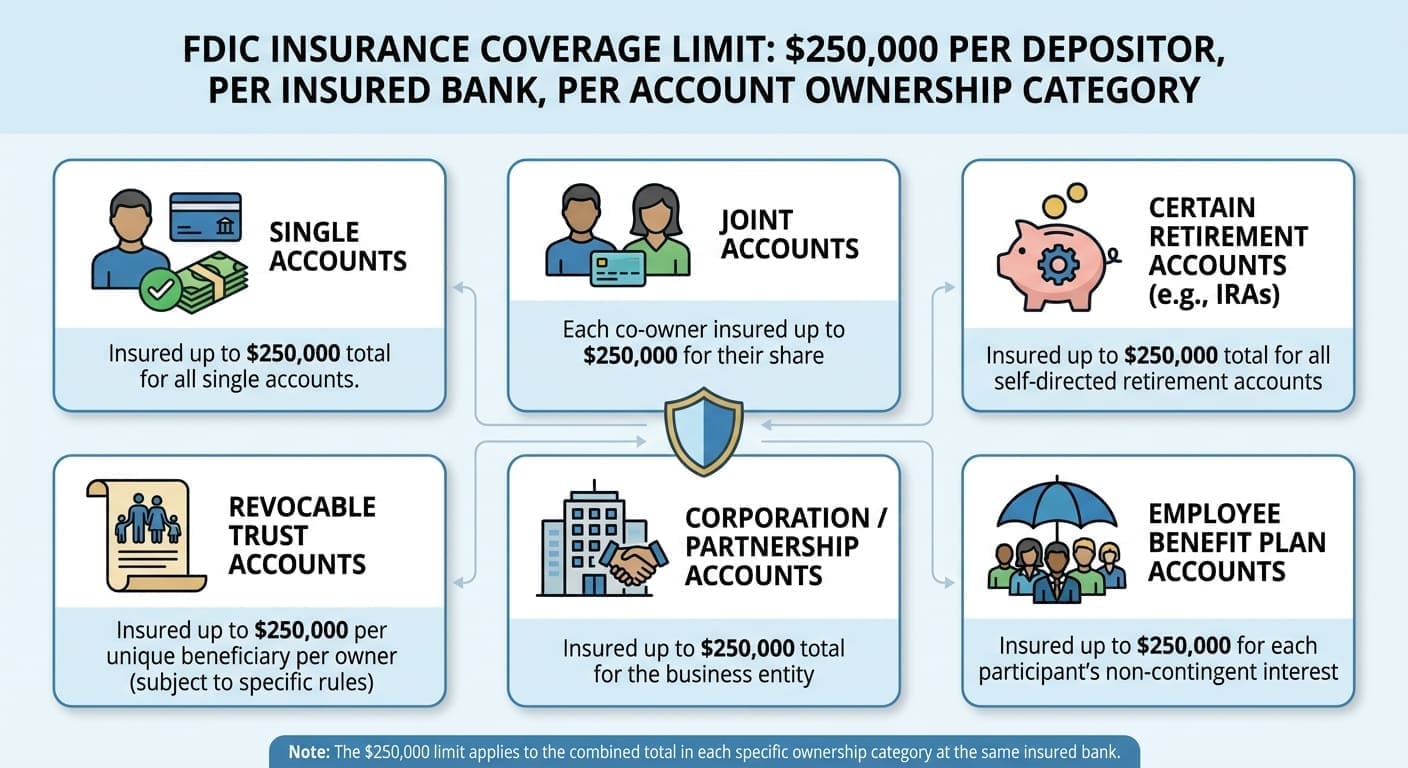

If the sponsor bank fails, the FDIC steps in to make you whole. The standard limit is $250,000 per depositor, per ownership category, at each insured bank.

Let us look at a quick numeric example. If you hold $300,000 in a single fintech app tied to one partner bank, $50,000 of your money is completely uninsured.

You must carefully track your total deposits across all platforms. If multiple apps use the same sponsor bank, those balances combine toward your single $250,000 limit.

The Synapse Bankruptcy Wake-Up Call

The financial world changed drastically after the Synapse bankruptcy in 2024. This middleware company connected dozens of fintech apps to actual banks.

When Synapse collapsed, the ledger systems tracking customer funds completely broke down. Partner banks could not verify who owned what portion of the pooled accounts.

Thousands of customers lost access to their money for months. The funds were stuck in regulatory limbo because the principal-agent relationship failed.

Listen closely: This event proved that pass-through insurance has a massive blind spot. The FDIC only protects against the failure of a bank, not the failure of a fintech intermediary.

If the app goes bankrupt, you are treated as an unsecured creditor. You might eventually get your money back, but it could take years of legal battles.

Regulators were stunned by the sheer complexity of the missing funds. It highlighted the severe dangers of relying on third-party software to manage bank ledgers.

You must acknowledge that middleware failures are a real threat to your liquidity. A high yield is never worth losing access to your emergency fund.

The FDIC insures deposits against bank failure, not against the failure of a non-bank fintech company. Consumers must understand this critical distinction.Federal Deposit Insurance Corporation Advisory

Are Neobanks Safe When Holding Crypto Assets?

Many modern financial apps offer both traditional deposits and cryptocurrency trading. This blending of services creates dangerous confusion for everyday consumers.

Here is the truth: Crypto assets held in any neobank account are never FDIC-insured. The government does not protect digital currencies under any circumstances.

Some companies have faced severe penalties for blurring these lines. The FDIC issued a cease-and-desist order to a prominent neobank for falsely implying crypto funds were secure.

You must mentally separate your fiat currency from your digital assets. Even if the app advertises a high APY, the underlying crypto investment carries total risk of loss.

If the platform gets hacked or goes bankrupt, your crypto is gone forever. There is no federal agency coming to rescue those specific funds.

Always read the specific disclosures regarding digital asset custody. The fine print usually reveals that a completely different, unregulated entity holds the crypto.

Mixing insured cash and uninsured crypto in one app requires extreme caution. Do not let a streamlined user interface trick you into a false sense of security.

Digital Banks vs Traditional Banks: Where is Your Money Most Secure?

Choosing between a digital startup and a legacy institution comes down to risk tolerance. Traditional banks hold their own charters and are directly regulated by the government.

When you deposit cash at a legacy bank, you deal directly with the insured entity. There is no middleman software company complicating the legal ownership of your money.

Many users wonder regarding digital vs traditional banks, which is better for large balances? The answer is almost always the traditional chartered institution.

However, digital apps often partner with multiple banks to offer extended coverage. Some platforms sweep your funds across four different banks to provide up to $1,000,000 in protection.

This multi-bank sweep model is clever but introduces multiple points of failure. You must trust that the fintech maintains perfect records across all four banking partners.

Traditional banks offer predictable safety without the technological gymnastics. You trade a slightly lower interest rate for absolute peace of mind.

Ultimately, traditional banks are safer because their legal structure is simple and tested. Complex fintech partnerships are still an unproven experiment in the eyes of many regulators.

How to Verify Your Fintech App is Actually Protected

You should never take an app marketing claim at face value. Finding the truth requires a little bit of digging into the legal fine print.

First, locate the exact name of the partner bank. You can usually find this at the very bottom footer of the company website or inside the app settings.

Next, verify that specific bank using the official FDIC BankFind tool online. If the partner bank is not listed there, close your account immediately.

You should also check the customer agreement for details on account structure. Ensure it explicitly states that funds are held in a custodial or fiduciary capacity.

If you are exploring options, reading a detailed Chime bank review can help you understand how established players handle these disclosures.

Pay attention to any emails about changes to the partner bank. Fintechs occasionally switch sponsors, which can temporarily disrupt your pass-through insurance coverage.

Always take screenshots of your monthly statements and account balances. If the app goes offline, you will need this proof to reclaim your funds from the partner bank.

- Locate the partner bank name in the footer.

- Verify the bank using the FDIC BankFind tool.

- Confirm the principal-agent legal structure in the terms.

- Monitor your email for partner bank changes.

- Keep total deposits under $250,000 per partner bank.

The Rise of Chartered Neobanks

Not all modern financial apps rely on the risky partner bank model. A select few have actually completed the grueling process of becoming real, chartered banks.

Companies like Varo and SoFi hold their own national bank charters. This means they are directly regulated by the OCC and carry their own FDIC insurance.

When comparing SoFi vs Ally, you are actually comparing two fully chartered institutions. The middleman risk is completely eliminated in these specific scenarios.

These chartered institutions offer the absolute best of both worlds. You get the sleek mobile experience of a startup with the rock-solid security of a legacy bank.

Obtaining a charter takes years and millions of dollars in legal fees. It shows a massive commitment to regulatory compliance and customer safety.

If safety is your absolute top priority, moving your funds to a chartered digital bank is a highly intelligent move. It removes the ambiguity of pass-through insurance.

You no longer have to worry about a middleware company collapsing. Your deposits sit safely inside an institution that answers directly to federal regulators.

What the 2026 Regulatory Wave Means for Your Wallet

The banking industry is facing a massive regulatory reckoning right now. Federal agencies are cracking down hard on the banking-as-a-service model to protect consumers.

We will likely see fewer new financial apps launching in the coming years. Sponsor banks are demanding much higher compliance standards from their technology partners.

This is ultimately a very positive development for everyday consumers. The apps that survive this wave will be significantly safer and more transparent.

If you are wondering is Chime safe today, the answer depends on their ongoing compliance efforts. Established players are investing heavily in legal teams to stay compliant.

You must remain proactive about where you store your cash reserves. Do not assume that every app on your phone is a safe place for your life savings.

Always keep your total deposits well below the $250,000 limit at any single institution. Splitting your emergency fund across different chartered banks is the smartest strategy.

Staying vigilant and informed is the only true way to protect your wealth. The future of digital finance is bright, but it requires you to read the fine print.

Frequently Asked Questions

Do neobanks have their own FDIC insurance?

No. Most neobanks are fintech companies, not chartered banks. They rely on partner banks to provide pass-through FDIC insurance for their customers.

What happens if a neobank goes bankrupt?

If the fintech app fails, your funds could be temporarily frozen while the partner bank reconciles the ledger. You are not protected by the FDIC against the failure of the app itself.

Is crypto held in a neobank insured?

No. Cryptocurrency is never insured by the FDIC. If the platform is hacked or fails, you could lose your digital assets entirely.

How can I verify my money is insured?

Check the app’s footer for the name of the partner bank, then search for that bank on the official FDIC BankFind tool to confirm its active status.

Are there any neobanks with real bank charters?

Yes. A few companies, such as SoFi and Varo, have successfully obtained national bank charters, meaning they carry direct FDIC insurance.