ⓘWritten and reviewed per our independent editorial methodology.

If you manage money on your phone today, you are participating in a massive financial shift. Navigating the choices requires understanding fintech vs digital banking perfectly. It is not just a battle over app features or sleek interface design. It is a fundamental difference in how your money is legally protected.

We spent the last decade building financial apps and testing the modern market. We tested exactly how these platforms handle real deposits, step-by-step. Our goal is to settle the fintech vs digital banking debate once and for all.

Money apps often look identical on the surface. However, looking at the underlying legal structure reveals a massive divide. Let us explore the precise differences in our 2026 guide.

Fintech and digital banking are often used interchangeably, but they are entirely different legal structures in 2026. Fintech refers to the technology driving financial services, while digital banking describes online-first neobanks that hold deposits. Understanding this difference dictates how your money is legally protected and insured.

- Fintech is the broad tech umbrella, while digital banking is a specific online banking model.

- Nonbank fintech apps rely on partner banks for deposit products and pass-through insurance.

- True neobanks offer branchless experiences with direct FDIC-insured deposit accounts.

- APY rates fluctuate heavily, with top digital banks offering up to 5.00% under strict conditions.

- Never keep large balances in payment apps without verified pass-through FDIC coverage.

Table of Contents

Quick Comparison: Fintech vs Digital Banking: The Key Differences in 2026 at a Glance

| Aspect | Fintech / payment apps | Digital banks (neobanks) |

|---|---|---|

| What it actually is | Technology software layer | Online-first banking provider |

| Who holds your money | A behind-the-scenes partner bank | Directly or via official partner bank |

| FDIC Insurance Status | Pass-through only (if applicable) | Direct or strict pass-through coverage |

| Best feature use case | Fast P2P payments and budgeting | Primary checking, salary DD, high APY |

| Current 2026 Examples | Cash App, Wise, PayPal | Chime, Varo, SoFi |

Exactly What is Fintech?

Fintech is the broad umbrella term for financial technology. It covers any technology-driven financial service or software layer. This includes everything from peer-to-peer payments to budgeting tools and open-banking software.

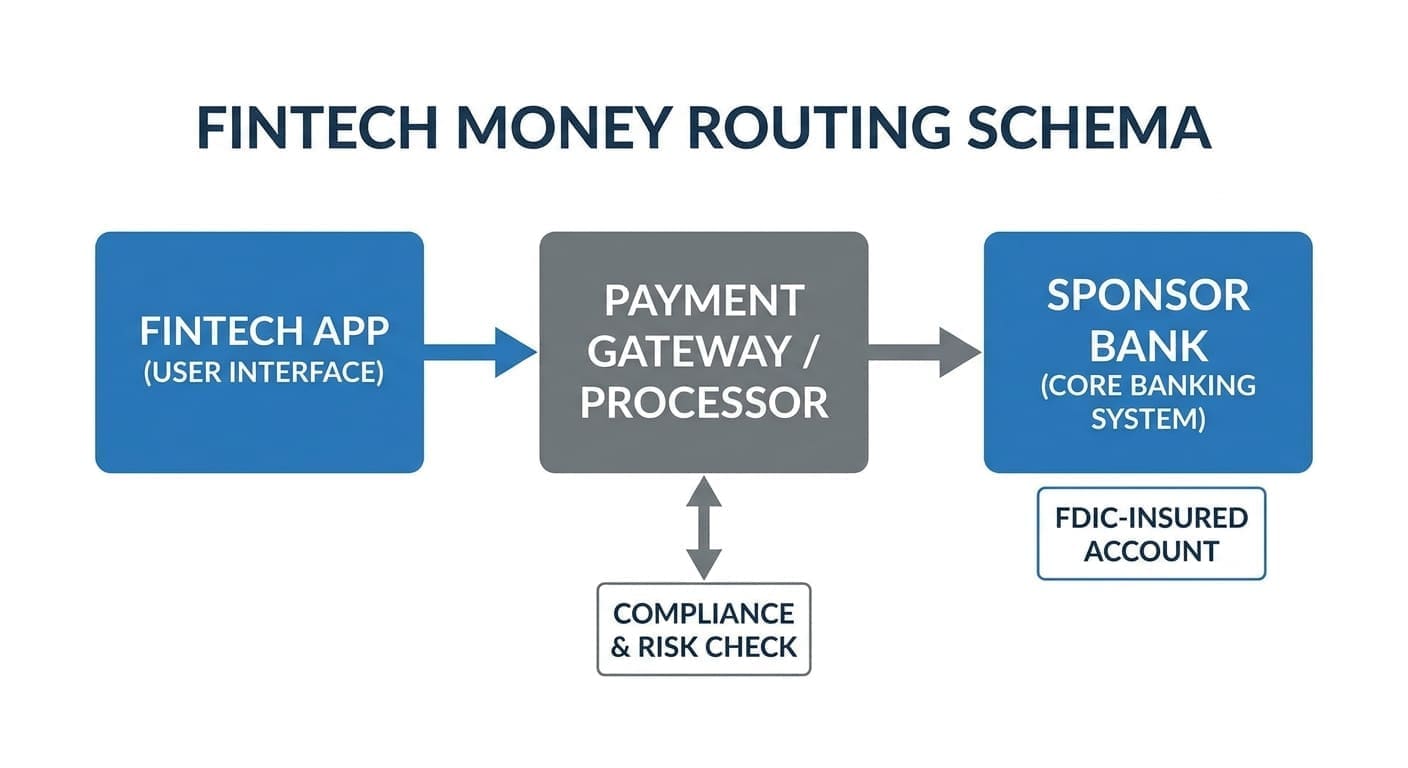

Many fintech companies do not hold a national bank charter. Instead, they act as the customer-facing software. They rely on traditional banks behind the scenes to actually hold user funds.

Popular Fintech Use Cases

- Quick peer-to-peer money transfers with friends.

- Automated expense tracking and budgeting tools.

- Specialized international money transfer networks.

- Investment platforms and fractional share trading.

Our take after testing dozens of these tools is that they focus on narrow, specific features. They want to make a single financial task incredibly easy. They do not want to become a full-service bank.

Where Fintech Falls Short

Fintechs are rarely built to be your primary checking account. Because they are not chartered banks, they cannot offer direct deposit insurance on their own balance sheet. Your money is entirely dependent on their backend banking partners.

If the tech startup fails, accessing your funds can be unnecessarily complicated. We saw this reality when Aspiration’s parent company filed for Chapter 11 bankruptcy in March 2025. This proves why you must be careful where you park your cash.

Exactly What is Digital Banking?

Digital banking is a specific banking channel. It refers to banks that deliver deposit accounts primarily or entirely online. When these institutions operate without any physical branches, they are often called neobanks.

Unlike an isolated payment app, a complete digital bank is responsible for your deposits. They handle compliance, bank regulation, and financial stability directly. To understand the full scope of these platforms, read our Ultimate Guide to Digital Banking.

The Core Features of a Neobank

- Primary checking and high-yield savings accounts.

- Debit cards with extensive fee-free ATM networks.

- Early salary direct deposit features.

- Direct or pass-through FDIC insurance coverage.

We constantly rely on these branchless options for everyday transactions. They offer higher interest rates by cutting the overhead costs of physical locations. They also eliminate the typical maintenance fees found at legacy street-corner banks.

Fintech vs Digital Banking: The Core Differences

The most critical distinction is regulatory status and deposit protection. A true digital bank or advanced neobank offers FDIC insurance on eligible deposits. A nonbank fintech app may only be a technology layer.

The debate over fintech vs digital banking ultimately comes down to legal ownership. Who actually holds your money? Let us break down the exact differences.

Understanding FDIC Insurance Reality

According to the FDIC insurance guidelines, standard US coverage limits remain $250,000 per depositor, per insured bank. This is absolute gospel for your emergency fund.

With a chartered digital bank, your money is directly protected. With a nonbank fintech, insurance depends entirely on pass-through coverage. This means the fintech must properly place your funds at an actual insured partner bank.

The Feature Differences

Fintechs prioritize speed and specific niche utility. They want you to send money to a friend in three seconds flat. They try to avoid the heavy regulatory burden of managing liquid assets.

Neobanks want your direct deposit. They want to be the hub where your salary lands every single month. To win that business, they offer advanced savings tiers and overdraft protection.

Comparing Top Platforms in the Fintech vs Digital Banking Space

We tested the biggest names in the industry to see how they perform in 2026. Our team analyzed their actual APY tiers, partner banks, and feature sets. Here is exactly where the top contenders fall in the fintech vs digital banking spectrum.

Chime: The Neobank Giant

Chime sits firmly in the digital banking category as a neobank partner. While technically a financial technology company, it offers full substitute banking services through The Bancorp Bank, N.A. and Stride Bank, N.A. (Members FDIC).

If you want the full breakdown of their features, check out our comprehensive Chime review.

What we liked

- They offer access to over 47,000 fee-free MoneyPass ATMs.

- SpotMe provides fee-free overdraft from $20 up to $200.

- Their savings tiers reward loyalty heavily.

The Savings Tiers Detail

Chime’s interest tiers require strict monthly activity. You get a basic 0.75% APY as the standard rate.

Upgrading to the Chime Plus tier gets you 3.00% APY, requiring $200 or more in qualifying monthly direct deposits. To reach the top 3.75% APY Chime Prime tier, you must hit $3,000 or more in monthly direct deposits.

Cash App: The Payment Fintech

Cash App is the ultimate example of a pure fintech tool expanding its footprint. It remains structurally a payment platform, utilizing Sutton Bank primarily as its card issuer.

For a deep dive into its spending tools, read our updated Cash App review.

Our take after testing

Cash App rules the peer-to-peer payment space effortlessly. However, it lacks a SpotMe-style free overdraft feature completely. It does offer a Borrow feature up to $500 based on eligibility, but that is a loan product, not standard overdraft.

Cash App Savings Structure

Cash App now offers legitimate balance-based savings, but you have to work for the interest. The base Cash App Savings yields 1.5% APY, provided you have a Cash App Card.

To unlock up to 3.25% APY, you must secure Cash App Green status. This requires either $500 in monthly card spend or qualifying direct deposits.

Fintech vs Digital Banking: Chime vs Cash App

When looking at fintech vs digital banking, this specific rivalry is the best case study. We detailed this heavily in our Chime vs Cash App comparison.

Chime wants to replace your old checking account entirely. Cash App wants to manage your casual spending and fast peer-to-peer transfers. They serve entirely different purposes based on their legal structures.

Varo: The Chartered Digital Bank

Varo is a fascinating player in the fintech vs digital banking discussion. Founded in 2015, they achieved a massive milestone by earning a national bank charter in 2020. This moved them from a simple fintech into a fully regulated digital bank.

Where Varo shines

Varo handles its own deposits directly without relying on backend partner banks. Their savings strategy is highly aggressive for lower balances.

They offer a 2.50% base APY on savings. However, they boost this to 5.00% APY on your first $5,000. To get this tier, you must secure $1,000 or more in qualifying direct deposits monthly and maintain a positive balance.

SoFi: The Comprehensive Alternative

We constantly look for stable options for our readers’ serious cash. How to Choose a High-Yield Savings Account is one of the most common questions we receive. SoFi currently dominates this specific category.

Who SoFi is for

SoFi is ideal for users seeking a highly stable, high-yield digital cash account. They offer up to 4.00% APY across Checking and Savings balances.

We absolutely recommend SoFi as a total replacement for unstable platforms like Aspiration. They feature over 55,000 fee-free Allpoint ATMs and include built-in Zelle functionality. They represent the high end of modern digital banking features.

The Real Economics of Digital Banking in 2026

The financial landscape has matured significantly over the last few years. According to Federal Reserve reports, consumer reliance on digital-first financial tools is at an all-time high. This makes understanding fintech vs digital banking mandatory for financial health.

Exploring Typical APY Ranges

Most high-yield digital cash accounts try to hover in the mid-4% to 5% APY range. These exact rates fluctuate based on federal policy.

True digital banks pass these yields down faster than traditional banks. Fintech platforms struggle to offer high yields without jumping through massive regulatory hoops. Always check the official provider sites for exact, up-to-the-minute numbers.

Understanding the True Fees

Both sides of the fintech vs digital banking spectrum market heavily around “no monthly maintenance fees.” Do not let this fool you into thinking they are charities.

Common charges still emerge quietly in specific interactions. You will often see out-of-network ATM fees if you stray from designated networks like MoneyPass or Allpoint. Instant-transfer fees and foreign transaction spreads are where these apps frequently make their profit.

“The lines between software and banking are blurring, but legal ownership of your deposits remains a stark dividing line.” – Jake Morrison

How to Choose the Right Platform

Deciding between fintech vs digital banking relies entirely on your personal cash flow. You cannot pick a platform just because the physical debit card looks cool. You must align the app’s structural strengths with your actual financial behavior.

We found that splitting your strategy often works best. You do not have to commit entirely to just one ecosystem.

When to Choose a Digital Bank

- You want a primary, everyday checking and savings relationship.

- You demand direct or secure pass-through FDIC insurance limits.

- You want all salary direct deposits and bill pay managed centrally.

- You want high APY yields tied to predictable direct deposit rules.

When to Choose a Fintech App

- You need to split dinner tabs with friends instantly.

- You want to track detailed budgeting across multiple external accounts.

- You are moving smaller amounts of casual spending money.

- You need cheap cross-border currency exchanges or international transfers.

The Global Perspective: UK and EU Markets

The fintech vs digital banking conversation looks different overseas. The regulatory environments in the UK and EU accelerated neobank adoption years ahead of the standard US market.

Starling and Monzo

In the UK, Starling Bank operates as a fully licensed traditional bank, wrapped in a digital-first app. They offer comprehensive FSCS protection up to £85,000.

Monzo remains incredibly popular with a 2.75% AER standard yield. If you upgrade to their Perks or Max tiers, you can push that to 3.25% AER. They also fall under the standard FSCS scheme.

Revolut and Monese

Revolut operates globally with heavy subscription tier models rather than strict lending goals. In the US, their Plus plan is $3.99, Premium is $9.99, and Metal is $16.99 monthly.

Monese is still operating actively across the UK and EU for multi-currency needs. They pivoted slightly into a broader general platform but remain vital for cross-border workers.

Summarizing Fintech vs Digital Banking

At the end of the day, fintech vs digital banking is a conversation about trust and legal boundaries. Fintech gives us the amazing software tools that make money move at lightspeed.

Digital banking provides the foundational security that actually lets us sleep at night. We highly suggest using an FDIC-insured digital bank for your core deposits. You can then safely link external fintech payment apps solely for convenience and speed.

By keeping these two concepts separate in your mind, you protect your wealth effectively. Make sure your primary cash sits with a chartered institution or a verified pass-through partner. Never assume an app is a bank just because it holds a balance.

The future of money is definitively digital. Ensure you are navigating this fintech vs digital banking ecosystem with absolute legally informed precision.