ⓘ Written and reviewed per our independent editorial methodology.

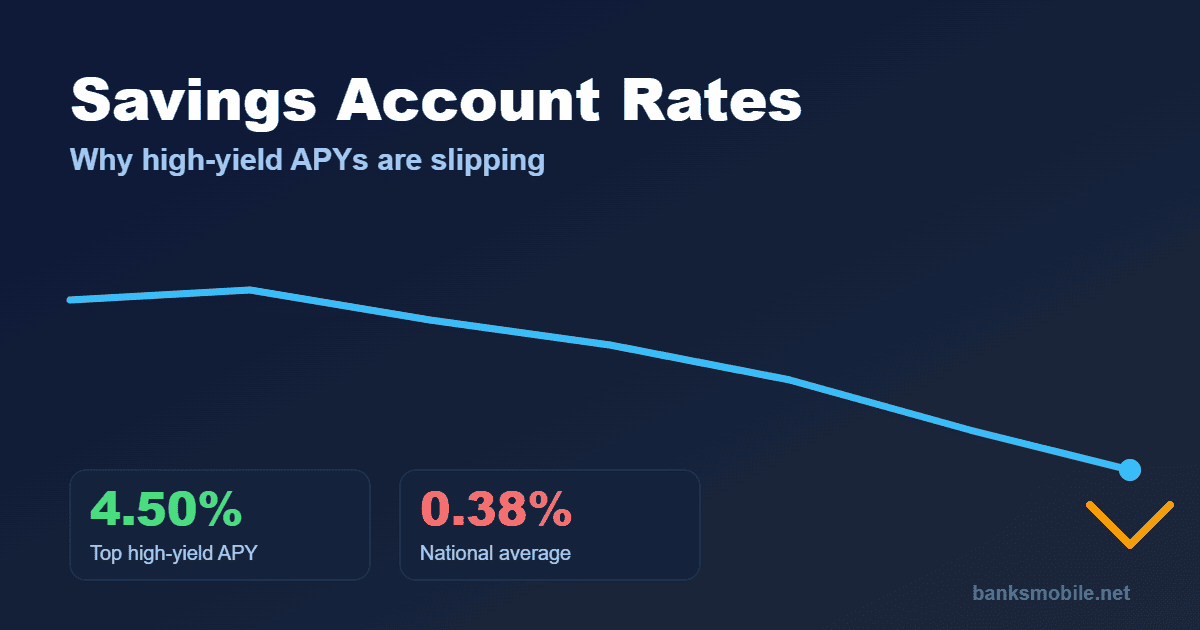

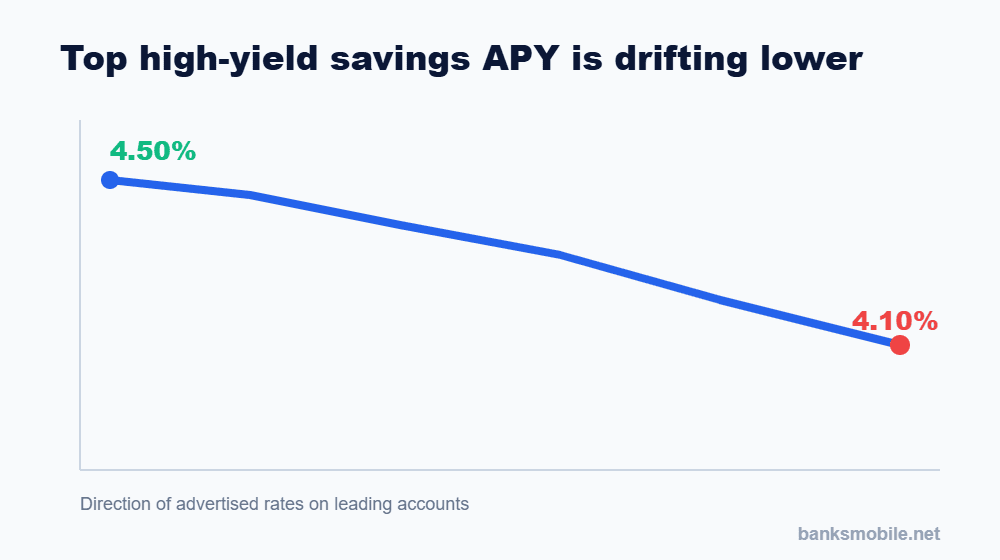

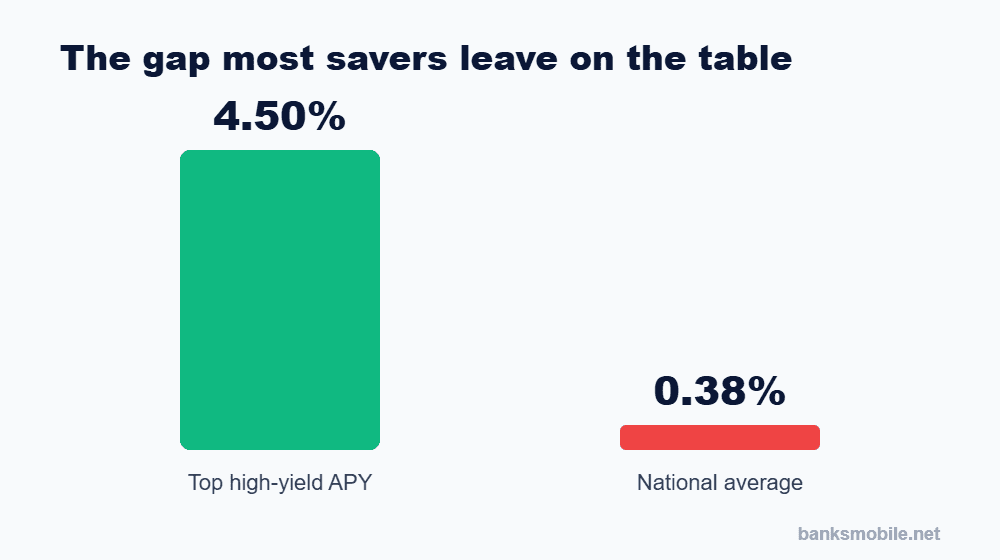

Yes, savings account rates are slipping in 2026, even though the Federal Reserve has kept its benchmark rate on hold. The best high-yield savings accounts still pay about 4.10% to 4.50% APY versus a 0.38% national average, but many banks have quietly trimmed their rates since spring. With the next Fed move leaning toward a hold or a hike rather than a cut, the smart play is to lock a strong rate now, either in a top high-yield savings account for cash you may need or a CD for cash you can set aside.

Savings account rates are quietly slipping in 2026, and the reason is not the one most savers expect.

The Federal Reserve has not cut its benchmark rate this year. It held steady again on June 17, keeping the federal funds target range at 3.50% to 3.75%, the fourth no change decision of 2026. Yet the interest banks actually pay on savings has still been drifting down. If you opened a high-yield account last year, the APY on it may already be lower than the number that first drew you in.

For anyone with cash parked in a savings account, this is worth understanding now rather than later. The gap between the best accounts and the national average has rarely been wider, and the direction of the Fed’s next move is not the one that would push savings rates back up. Below, we break down what is happening, why it is happening even with the Fed on hold, and the practical moves that make sense while rates are in motion. Run the math on your own balance as we go, because the right call depends on it.

- The Federal Reserve held its benchmark rate steady on June 17, 2026, keeping the target range at 3.50% to 3.75%.

- Even so, savings account rates have drifted lower: of 14 tracked high-yield accounts, 11 cut their APY since early May and only 3 raised it.

- The best high-yield savings accounts still pay roughly 4.10% to 4.50% APY, versus an FDIC national average of just 0.38%.

- Markets expect the Fed to stay on hold at its July 29 meeting, with the next move leaning toward a hike rather than a cut.

- Lock a rate now: a top high-yield savings account for liquid cash, or a CD for money you can set aside.

Why savings account rates are slipping in 2026

Here is the part that confuses people: banks do not set deposit rates off today’s Fed level alone. They price them off where they expect rates to go, how badly they need your deposits, and how much margin they want to protect. All three of those inputs have shifted this year, and all three point the same way, which is down.

First, expectations. With the labor market cooling through the first half of 2026, markets have penciled in eventual rate cuts, even if they are further out than savers hoped. Banks do not wait for the Fed to act before they start trimming. Second, competition has eased. The wave of cash that flooded into high-yield accounts when rates first jumped has slowed, so banks no longer have to fight as hard for every dollar. When a bank does not need to lure deposits, the easiest lever it pulls is the advertised APY. If you are still fuzzy on what that number even means, our explainer on what APY is and how it is calculated breaks it down.

The data backs it up. Across 14 widely tracked high-yield savings accounts, 11 lowered their APY since early May and only 3 raised it. Month to month the drift looks small, a tenth of a percent here, a quarter point there. Run the math over a year on a real balance, though, and it adds up, especially when several small cuts stack on top of each other. This is exactly why parking cash and forgetting about it is the quiet tax most savers pay. Our guide to how high-yield savings accounts work covers the mechanics if you want the full picture.

What the Fed did, and what comes next

On June 17, 2026, the Federal Open Market Committee left the federal funds rate unchanged for the fourth meeting in a row, holding the target range at 3.50% to 3.75%. The effective rate sits near 3.63%. That is the number every savings and CD rate ultimately keys off, so the fact that it has not budged is why top accounts still pay in the low to mid 4 percent range rather than collapsing.

The next decision lands on July 29, 2026. Markets put the odds of no change near 89 percent, with a small chance of a hike and almost no chance of a cut. That last point matters more than it sounds. The Fed’s June projections nudged the year end outlook higher, so the risk now leans toward one more hike rather than the cut savers were hoping would lift their yields. Futures pricing points to a path drifting toward roughly 3.8 percent by October and close to 4 percent around year end. In plain terms, nobody should be waiting on the Fed to rescue their savings rate this year.

Where rates stand right now

Here is a snapshot of where the key numbers sit in early July 2026. The spread between a top account and the national average is the headline: the best accounts pay more than ten times what the typical bank hands out, and the FDIC national average shows just how little most savers earn by default.

| Benchmark | Current level |

|---|---|

| Top high-yield savings APY | ~4.10% to 4.50% |

| FDIC national savings average | 0.38% |

| Fed funds target range | 3.50% to 3.75% |

| Top 1-year CD APY | ~4.00% to 4.40% |

| Tracked high-yield accounts, change since May | 11 lowered, 3 raised |

The Fed is on hold, but your bank is not waiting for it to move.

What slipping rates mean for your money

Put real numbers on it. On a $10,000 balance, a 4.40% APY earns about $440 over a year. The same $10,000 in an account paying the 0.38% national average earns about $38. That is a $402 gap for doing nothing more than choosing a better account. This is the single most valuable move most savers can make, and it costs nothing but a few minutes.

Now layer in the drift. If your account quietly trims its APY by a quarter point, that is $25 a year on $10,000, small on its own but compounding over time and across a larger balance. You can see how the compounding plays out with our compound interest calculator, or map a specific goal with the savings calculator. The real risk is not the small cut, it is complacency, leaving an emergency fund in a legacy account earning close to zero while the top of the market pays more than 4 percent.

Cash sitting in a top high-yield account keeps earning near the ceiling of the market, even as rates ease. On $20,000 that is roughly $880 a year, real money that compounds.

EARNING 4% AND UPThe same $20,000 in a legacy account at the 0.38% average earns about $76 a year. After inflation, its buying power quietly shrinks while it sits there.

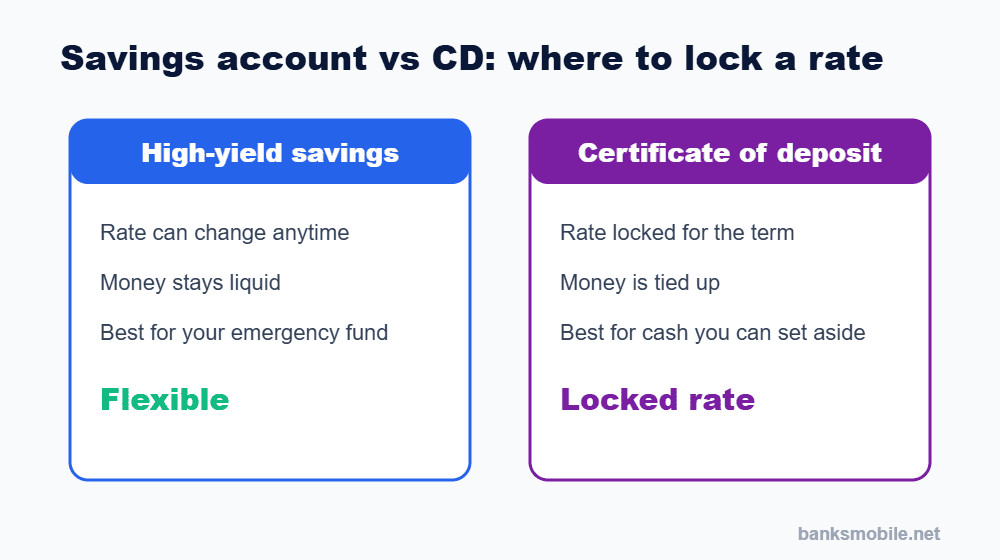

EARNING NEAR ZEROSavings account vs CD: where to lock a rate

When rates are drifting down, the question is not only which account pays the most today, but which one protects the rate you get. That is the real difference between a high-yield savings account and a certificate of deposit. A savings account keeps your money liquid, but its rate can change any day. A CD locks a fixed rate for a set term, so a cut cannot touch it, but your cash is tied up until the CD matures.

The practical split is simple. Keep your emergency fund and any cash you might need in a high-yield savings account, where you can reach it without penalty. Take money you know you will not touch for a year or more, and lock it in a CD near 4.40% while that rate is still on offer. Before you commit, run both options through our CD calculator and size your safety net with the emergency fund calculator so you never lock up cash you actually need.

What to do right now

- Confirm the account is FDIC insured (or NCUA for a credit union).

- Check whether the top APY has a balance cap.

- Verify there is no monthly fee or minimum that eats the interest.

- Keep at least three to six months of expenses liquid before locking a CD.

- Confirm the live APY on the provider site, since rates change often.

If you are still deciding where to keep your money day to day, our comparisons of SoFi versus Ally and the best online banks like Chime walk through the accounts that consistently pay near the top of the market. You can also run every scenario through our full set of free banking calculators, or brush up on the basics with our guide to APY and how it compounds.

Savings account rates are drifting lower in 2026 even though the Fed has not moved, and the direction of the next move is not down. If a strong rate matters to you, the window to lock one is now, not after a cut. The number that decides your move is your balance and your timeline: liquid money belongs in a top high-yield savings account, and cash you can set aside belongs in a CD at today’s rate.

Frequently asked questions

Are savings account rates going up or down in 2026?

They are trending slightly down. Of 14 tracked high-yield accounts, 11 lowered their APY since early May and only 3 raised it, even though the Fed held its benchmark rate steady.

Why are savings rates falling if the Fed has not cut?

Banks price deposits on expectations and competition, not just the current Fed level. With markets expecting eventual easing and deposit competition cooling, some banks trimmed APYs to protect their margins.

What is a good savings account rate right now?

The best high-yield savings accounts pay roughly 4.10% to 4.50% APY, far above the FDIC national average of 0.38%. Anything below about 4 percent is worth a second look.

Should I open a CD before rates drop?

If you can set the money aside, a top 1-year CD near 4.40% locks today’s rate. Keep any cash you might need soon in a liquid high-yield savings account instead.

Will the Fed cut rates at its July 2026 meeting?

Markets put the odds of a cut on July 29 near zero. The Fed is expected to hold, and its own projections lean toward a possible hike rather than a cut.

Is my money safe in a high-yield savings account?

Yes, as long as the account is held at an FDIC insured bank or an NCUA insured credit union, your deposits are protected up to $250,000 per depositor, per bank, per ownership category.