ⓘWritten and reviewed per our independent editorial methodology.

Let us cut straight to the chase about your idle cash. If your money is sitting in a basic account at a traditional physical bank, inflation is actively eating up your wealth. This harsh reality leads many everyday savers to ask exactly what is a high-yield savings account, and how can it protect my money? The good news is that upgrading your cash strategy is incredibly simple.

We frequently test checking and savings products to see which institutions genuinely prioritize your wealth. Time and time again, we find that migrating your cash to a modern bank yields massive dividends. When we break down exactly what is a high-yield savings account, we see a totally risk-free tool that pays out real money every month.

Our team has spent hundreds of hours analyzing interest rates and consumer data for 2026. We are ready to explain everything you need to know about these accounts. Read on as we define what is a high-yield savings account, compare the best options, and show you precisely how to accelerate your financial goals.

A high-yield savings account (HYSA) is a deposit account that pays significantly higher interest rates than traditional banks while keeping your money safe and accessible. By eliminating physical branch costs, online banks can offer APYs up to 20 times the national average. These accounts are fully insured up to $250,000, making them a cornerstone of any wealth-building strategy.

- Earn 10x to 20x the national average on your cash.

- Access top APYs ranging from 4.00% to 5.00% in 2026.

- Money is never locked away; withdraw funds anytime.

- Online banks pass branch overhead savings to you.

- Deposits are safely insured by the FDIC up to $250,000.

Table of Contents

Switching to a high-yield savings account is the single easiest way to give your idle cash an immediate, risk-free promotion.

What Is a High-Yield Savings Account? A Complete Guide at a Glance

| Account type | Typical APY | Access to cash | Best for |

|---|---|---|---|

| Standard savings account | 0.01% – 1.6% (2026 avg) | High (branches + online) | In-person banking lovers |

| High-yield savings account | 4.00% – 5.00% (2026 top) | High (online focus) | Emergency funds & short goals |

| Money market account | Similar to HYSA top rates | High (includes checks/cards) | Savers needing check writing |

| Certificate of deposit (CD) | 4.00% – 5.00%+ (fixed) | Low (locked for term length) | Guaranteed specific yields |

Understanding the Basics: What Is a High-Yield Savings Account?

An HYSA is essentially a standard savings account with a massively supercharged, variable interest rate. From a regulatory perspective, there is no legal difference between an HYSA and a traditional savings account. Both are simply “savings accounts” governed under the same banking laws.

However, the term “HYSA” is used as a specific marketing label for accounts offering Annual Percentage Yields (APYs) roughly 10 to 20 times the national average. When people ask what is a high-yield savings account legally, the answer is just a normal savings account that actually pays you fairly. They are primarily offered by online-only banks, neobanks, and forward-thinking credit unions.

How Does It Work?

You deposit money into the account, and the bank pays you a percentage of your balance as interest. Unlike Certificates of Deposit (CDs), your money is not locked for a set term. You maintain the freedom to transfer or withdraw funds whenever you face an unexpected expense.

APY vs. National Average Rates

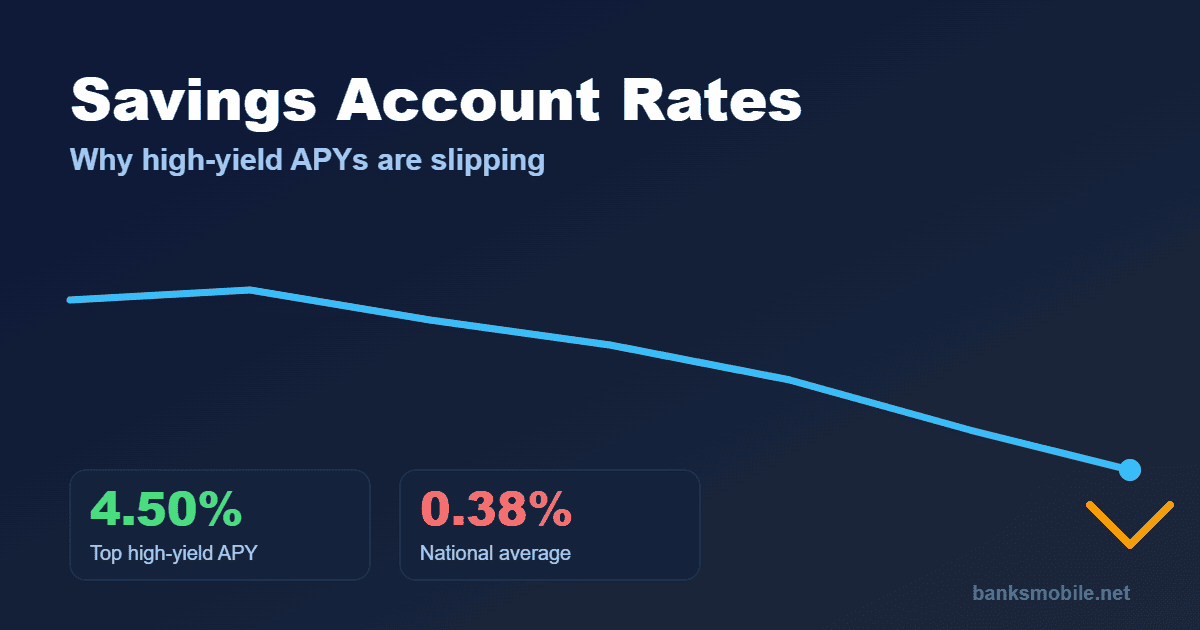

To truly grasp what is a high-yield savings account, you have to look at the math. As of June 2026, the best HYSAs offer APYs ranging from 4.00% to 5.00%.

Meanwhile, the national average for savings accounts sits at approximately 1.6%. When you look closer at specific traditional brick-and-mortar institutions like Chase or Bank of America, the reality is even starker. These physical banks offer yields of less than 1%, frequently bottoming out at 0.01%.

The Mechanics Behind What Is a High-Yield Savings Account

Many consumers wonder if these high rates are a scam or a temporary trick. They are neither. The explanation for these impressive APYs is simple arithmetic related to business overhead costs.

- Why Online Banks Pay More. Physical branch networks require massive capital. Traditional banks pay for prime real estate, utility bills, maintenance, and vast teams of in-person tellers. Online banks simply skip these expenses. If you read our guide on Digital vs Traditional Banks, you will see the exact financial breakdown. Online platforms take the money they save on overhead and pass it directly to you via higher interest rates. This efficient business model is the core of what is a high-yield savings account today.

- The Power of Daily Compounding. Compounding is the secret engine of wealth creation. This happens when the interest you earn is added directly to your principal balance. The following month, your future interest is calculated on that new, larger total. Most modern high-yield accounts compound your interest daily, then pay it out monthly. The more frequently interest is compounded, the faster your money grows. If you want to see exactly how your money responds, try running your numbers through our Compound Interest Calculator.

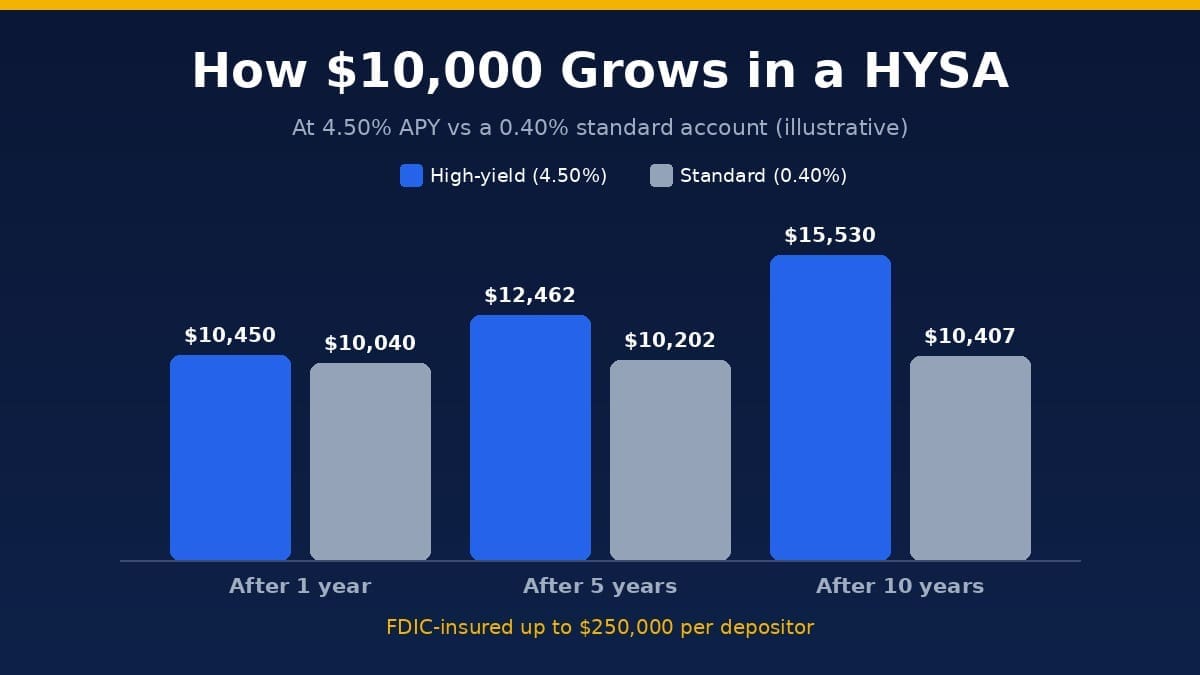

- Concrete Worked Example. Let us look at a real-world scenario to make this concept crystal clear. Say you deposit $10,000 in an account paying 4.50% APY. Because APY already includes compounding, after one year you earn $450 in interest, growing your balance to $10,450 – all without lifting a finger. By comparison, if that same $10,000 sat in a traditional bank at 0.01%, you would earn roughly $1.00 over the entire year.

Pros and Cons of a High-Yield Savings Account

Every financial product has tradeoffs. While we heavily advocate for transferring idle cash to a high-rate account, we always evaluate both sides of the coin.

Before deciding entirely what is a high-yield savings account good for, weigh these core benefits and drawbacks.

Where HYSAs Shine

- High Returns: You earn exponentially more interest than a standard bank offers.

- Absolute Safety: Zero exposure to stock market volatility or crypto crashes.

- Full Liquidity: You can pull your cash out for emergencies at almost any time.

- Zero Maintenance Fees: Most modern digital platforms charge zero monthly fees.

Switching to a high-yield savings account is the single easiest way to give your idle cash an immediate, risk-free promotion.

Where HYSAs Fall Short

- Variable Rates: Interest rates fluctuate based on decisions made by the Federal Reserve. They can rise or fall with the broader economy.

- No Cash Deposits: Without physical branches, depositing physical paper money is often complicated or impossible.

- Transfer Delays: Moving funds back to your primary checking account might take 1 to 3 business days.

Our Top Picks: Exploring What Is a High-Yield Savings Account in 2026

We tested dozens of accounts to see which platforms actually deliver on their promises. While reviewing what is a high-yield savings account across the market, stability and historical reliability mattered heavily to us. We highly advise against chasing unstable platforms-for instance, we no longer recommend Aspiration since their parent company filed Chapter 11 in 2025.

Instead, focus on these verified, trusted institutions offering stable yields as of June 2026.

SoFi Checking & Savings

SoFi remains an incredible overall banking hub for digital consumers. They effectively replace outdated platforms. Right now, SoFi offers up to 4.00% APY across checking and savings balances.

They also provide a massive fee-free ATM network via Allpoint with 55,000+ locations. If you need a fully integrated system with Zelle built directly into the app, SoFi is highly capable.

Marcus by Goldman Sachs

If you want the backing of a Wall Street titan, Marcus offers a phenomenal standalone savings product. You can check the current official rates directly at Marcus by Goldman Sachs.

As of June 2026, Marcus provides a solid 3.40% APY. They focus entirely on straightforward saving and investing tools, meaning there is no checking account attached. It perfectly serves users who want their savings somewhat separated from their daily spending.

Ally Bank

Ally Bank is one of the original pioneers of online banking. They consistently offer competitive rates, currently providing a 3.00% APY on their standard savings product.

We love Ally for their unique “Savings Buckets” feature. This tool allows you to visually divide your single account balance into distinct goals, like an emergency fund, a vacation fund, or car repairs.

Chime and Varo (For Active Spenders)

If you primarily use neobanks for everyday transactions, you can unlock tiered savings. Chime offers a 0.75% standard APY up to a 3.75% APY on their Chime Prime tier, requiring $3,000+ in monthly direct deposits.

Varo also rewards active users. You get a 2.50% base APY, but if you secure $1,000 in monthly direct deposits and maintain a positive balance, they boost you to 5.00% APY on your first $5,000.

How to Choose What Is a High-Yield Savings Account Best for You

Selecting the right bank comes down to your personal workflow. Not all accounts are created equally, even if they boast similar interest rates.

If you want a detailed breakdown of rating methodologies, check out our guide on How to Choose a High-Yield Savings Account. In the meantime, evaluate candidates using the following strict criteria.

Essential Criteria to Evaluate

- Consistent APY History: Do they drop their rates the moment they acquire enough customers? Look for long-term consistency.

- Monthly Maintenance Fees: Never pay a fee to save your own money. The best platforms charge $0.

- Minimum Balance Requirements: The top accounts require no minimums to open or to earn the highest APY tier.

- App Experience: Since you lack physical branch access, the mobile app must be highly intuitive and bug-free.

Are High-Yield Savings Accounts Safe?

A core part of defining exactly what is a high-yield savings account involves understanding the underlying protections. People are notoriously skeptical of online banks without a brick-and-mortar presence.

Fortunately, your money is just as secure online as it is down the street. Federal insurance is the golden standard for banking confidence.

Understanding FDIC Insurance

If an institution is a registered member of the FDIC, your money is protected if the bank collapses. Coverage provides up to $250,000 per depositor, per insured bank, per ownership category. You can verify any bank’s official insured status directly via FDIC.gov.

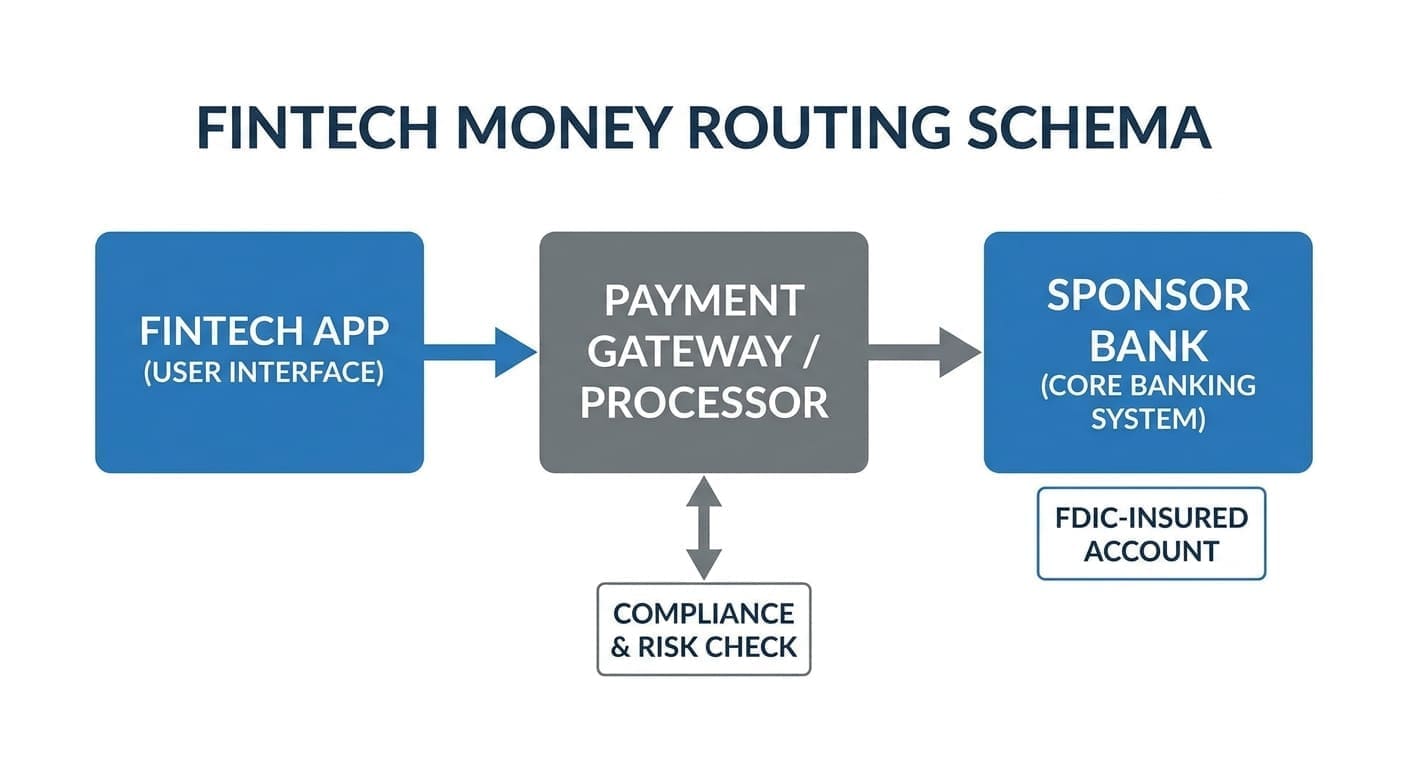

If you use a financial technology company or neobank (like Chime), your money is often swept to partner banks. For example, Chime partners with The Bancorp Bank, N.A. and Stride Bank, N.A. (both Members FDIC). Always confirm where your money actually sleeps.

Using Calculators to Predict Your Growth

Predicting your wealth journey should rely on math rather than emotion. Once you secure an account, map out your future using data-driven projections.

We highly recommend utilizing our Savings Calculator to forecast regular monthly deposits. By plugging in your starting balance, intended monthly contribution, and your new APY, you can visualize exactly when you will hit your emergency fund goals.

If you want to evaluate loans or large purchases alongside your savings efforts, browse our suite of Free Financial Calculators. Being organized is half the battle in personal finance.

Final Verdict on What Is a High-Yield Savings Account

As we wrap up our intensive review for 2026, the question of what is a high-yield savings account is easily answered. It is the absolute optimal landing spot for your daily cash reserves.

By blending total liquidity with impressive interest, you defend your purchasing power against inflation. Do not let traditional banks pay you pennies while using your capital to fund their own investments. Make the pivot to a modern digital platform, secure your FDIC insurance, and start earning the yields you rightfully deserve.