ⓘWritten and reviewed per our independent editorial methodology.

Standing in line at a physical bank branch feels like a massive step backward for most modern consumers. The rise of digital banking has fundamentally altered our checking and savings habits over the past decade. We test financial apps daily, and the shift away from brick-and-mortar institutions is permanent.

Our team has spent thousands of hours reviewing modern fintech infrastructure. As a former fintech founder, I watch how digital banking continues to refine its offering with tiered high-yield savings and zero-fee access. Whether you want to escape steep monthly maintenance charges or lock in competitive interest rates, making the digital jump is often highly profitable.

This guide breaks down everything you need to know about navigating digital platforms in 2026. We look at exact yield tiers, strict direct deposit conditions, and hidden pitfalls to avoid. Our goal is to help you easily choose an account that maximizes your cash without stressing over fine print.

- Digital banks offer higher yields and lower fees than traditional brick-and-mortar institutions.

- Understand APY requirements, like Chime Prime’s $3,000/mo deposit for top tier yields.

- Always verify FDIC insurance coverage up to $250,000 per depositor.

- Avoid unstable platforms; we replaced Aspiration in our recommendations with stable options like SoFi.

- Assess specific app tiers (Revolut, Monzo) to match subscription costs to your daily financial needs.

Table of Contents

The Evolution of Digital Banking in 2026

Digital banking is no longer a niche alternative for early tech adopters. These platforms, often referred to as neobanks or online-only banks, primarily operate exclusively through responsive apps and websites. Because they avoid the massive overhead costs of real estate and branch networks, they pass those savings directly to depositors.

For a U.S. and global audience in 2026, the distinctions are clearer than ever. App-based accounts feature branchless access, intuitive money management interfaces, and almost universally lower fees compared to traditional giants. More importantly, they frequently offer significantly higher deposit rates on standard checking and savings products.

What Exactly Qualifies as a Neobank?

Neobanks are banking providers engineered specifically for mobile-first users. Account origination, scheduled transfers, card freezing controls, and customer support are handled entirely from your phone. You never have to sit at a desk with a loan officer.

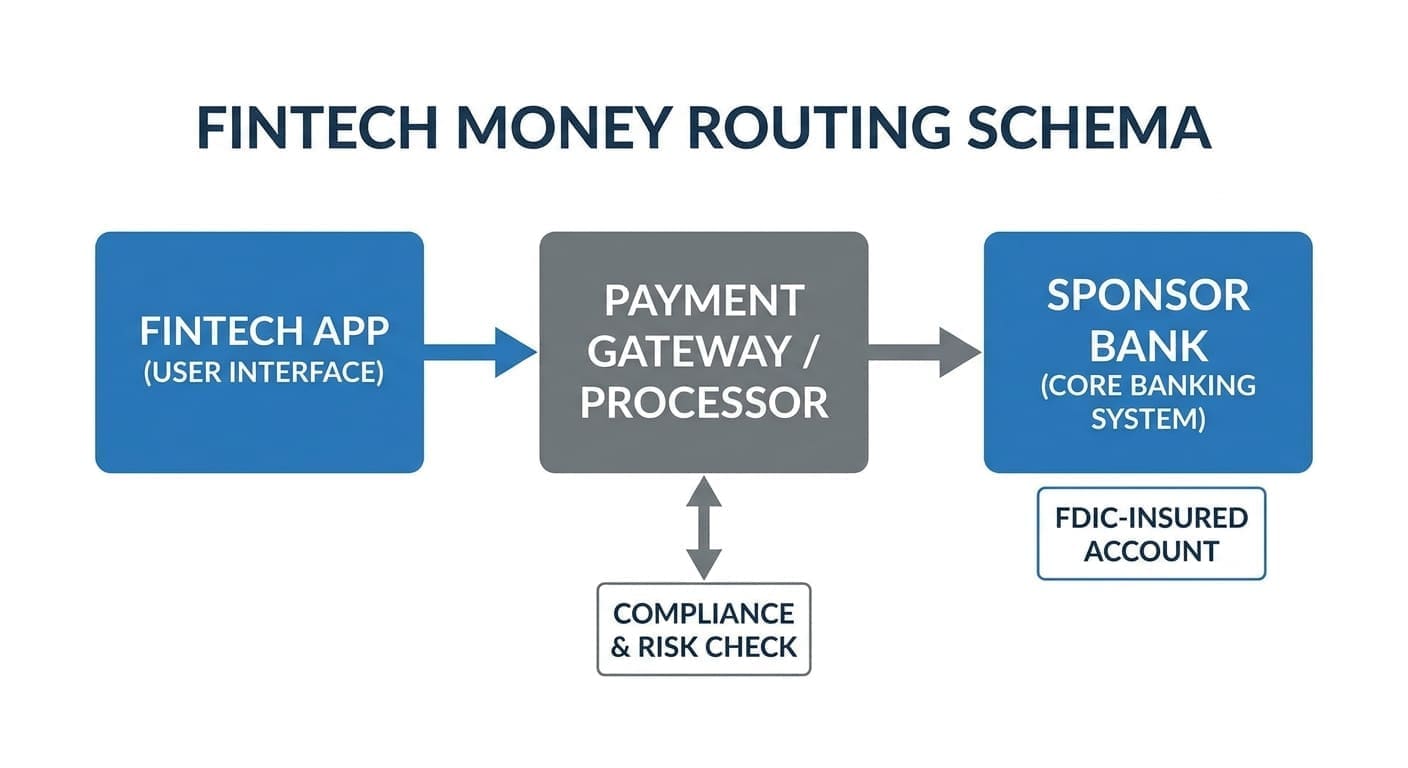

Behind the scenes, many neobanks partner with chartered institutions to hold your funds legally. For instance, The Bancorp Bank, N.A. and Stride Bank, N.A., partner with various top-tier apps to ensure your money remains secure. Others have fought to secure their own national banking charters to operate completely independently.

Traditional versus Digital Providers

Traditional financial institutions boast thousands of physical branches, massive proprietary ATM grids, and complex suites of localized lending products. They cater to small businesses needing daily coin deposits or consumers wanting face-to-face mortgage advice. However, this vast footprint forces them to maintain higher fee structures.

Conversely, a digital banking provider emphasizes stark app convenience and low-cost operations. They suit individuals who are highly comfortable managing cash flows online and who want zero monthly maintenance fees. If you rarely deposit physical paper cash, the online route typically saves you hundreds of dollars annually.

Top U.S. Digital Banking Providers We Tested

The American market offers a fiercely competitive lineup of online checking and savings accounts. We actively track shifting Annual Percentage Yields (APYs) and the exact conditions required to earn them. Below are the definitive front-runners we recommend for 2026.

Chime: Tiered Savings and No Hidden Fees

Founded in 2013, Chime remains a heavyweight champion in the online checking space. We recently completed a detailed Chime review assessing their new 2026 tiered structure. The company partners directly with The Bancorp Bank, N.A. and Stride Bank, N.A. (Members FDIC) to protect your deposits.

Chime offers a massive network of 47,000+ fee-free MoneyPass ATMs. They are famous for their SpotMe feature, which provides fee-free overdraft coverage ranging from $20 to $200 based on your account history and direct deposits. Their savings yield structure is heavily tiered based on your primary account activity.

- Standard Saving: 0.75% APY standard out of the box.

- Chime Plus: Earn 3.00% APY. Requires $200+ per month in qualifying direct deposits (or $400 combined over 34 days).

- Chime Prime: Unlock 3.75% APY by depositing $3,000 or more each month via qualifying direct deposits.

Cash App: Hidden Savings Powerhouse

Cash App has aggressively expanded beyond simple peer-to-peer sending into a full financial hub. Their card issuer is Sutton Bank, bringing reliable infrastructure to your daily spending. Readers frequently ask about Cash App features in our Cash App review, specifically regarding their savings tiers.

Cash App Savings is a real, balance-based savings feature offering a 1.5% base APY simply by owning the Cash App Card. You can elevate this yield up to 3.25% APY by achieving Cash App Green status. Getting Green requires either $500 or more in monthly card spend or qualifying direct deposits.

Varo: High Rate on Capped Balances

Varo transitioned in 2020 by acquiring its own national bank charter, making it a rare independent neobank. We consistently compare Chime vs Varo because both cater to fee-conscious spenders. Varo uses a tiered incentive model to reward loyal customers with incredible top-end rates.

Varo pays a respectable 2.50% base APY right out of the gate. However, if you clear $1,000 or more in monthly qualifying direct deposits and keep your balance positive, you earn a massive 5.00% APY on your first $5,000. It is an unmatched return if you keep your emergency fund right around that five-grand threshold.

Ally Bank: The Classic High-Yield Standard

Ally Bank is essentially the godfather of modern high-yield internet banking. If the tiered hurdles of neobanks annoy you, Ally offers a straightforward, branchless checking and savings suite. Our Chime vs Ally comparison highlights that Ally appeals primarily to established savers who want simple terms.

As of June 2026, Ally offers a solid 3.00% APY on savings balances with zero monthly maintenance obligations. Their app features clever saving buckets and surprise savings algorithms that automate your financial growth. They remain a totally reliable, gimmick-free zone.

High-Yield Digital Banking Options Compared

The real allure of stepping away from national brick-and-mortar brands is locking in superior interest for your idle cash. If your focus in digital banking is purely on maximizing safe yield without risking the stock market, you have fantastic options. We track these base rates directly to cut through marketing noise.

Top Contenders for Idle Cash

Beyond Ally, several massive institutions have shifted their weight into online-only high-yield branches. They lack the budgeting gamification of Chime, but they drastically outpace neighborhood branch yields. Here is exactly what we are seeing across the board in 2026:

- Marcus by Goldman Sachs: 3.40% APY on their simple High-Yield Online Savings platform as of June 2026.

- Discover: Up to 3.50% APY with incredible 24/7 localized customer service.

- Capital One 360: Currently paying out a flat 3.00% APY.

- SoFi: Easily the most aggressive all-in-one platform, pushing up to 4.00% APY across their combined Checking and Savings product.

A Critical Note on Aspiration

We must directly address a past favorite among green-focused savers. Parent company Aspiration Partners officially filed for Chapter 11 bankruptcy in March 2025 and moved rapidly into liquidation. The consumer brand was spun off to new ownership, but the operational footing remains highly unstable.

We no longer recommend Aspiration as a stable high-yield account, and there is no reliable or officially guaranteed current APY available. If you loved their mission and rates, we strongly suggest porting your funds to SoFi immediately. Your digital banking setup must be rock solid above all else.

Global and Multi-Currency Digital Banking Leaders

Our readers increasingly travel, freelance globally, or send remittances across borders. A localized checking account usually penalizes international behavior with steep foreign transaction fees and brutal exchange margins. The global neobank sector fixes this issue entirely.

Revolut: The All-in-One Global App

Revolut is a true financial monolith for digital nomads. The app lets you hold dozens of currencies simultaneously and exchange them at phenomenal interbank rates. They utilize a distinct subscription-based model that differs depending on which side of the pond you live on.

In the US, Revolut offers three distinct personal plans:

- Plus ($3.99/mo)

- Premium ($9.99/mo)

- Metal ($16.99/mo)

In the UK, the platform expands heavily with localized perks and travel insurance bundles. British users access Plus (£3.99), Premium (£7.99), Metal (£14.99), or the massive Ultra tier (£55/mo). Before paying, ensure your monthly foreign exchange volume actually justifies the subscription fee.

Monzo and Starling: The UK Rivals

The UK essentially invented the modern multi-currency personal app. When reviewing Starling vs Monzo, we look at two institutions that are fully licensed UK banks protected by the FSCS up to £85,000. They have essentially conquered the London commuter market.

Monzo currently offers a 2.75% AER standard rate. You can push this right up to 3.25% AER if you upgrade to their Perks or Max tier memberships. Starling Bank continues to hold its own by offering exceptional business accounting integrations without the dizzying array of paid personal tiers.

Wise: The Kings of Remittance

Wise operates uniquely in the digital banking ecosystem. While they offer a multi-currency holding account and debit card, they are fundamentally an international transfer powerhouse. They pride themselves on absolute transparency regarding mid-market exchange rates.

We love their fee structure. Transfers typically run from 0.45% to 0.65% on major currency pairs, occasionally reaching up to ~2% on exotic currencies. The base rate sits around ~0.33% alongside a tiny fixed execution fee, totally undercutting traditional international wire charges.

Features Often Confused with Bank Accounts

Not every financial icon on your smartphone represents a real, insured deposit institution. The rapid expansion of fintech has blurred the lines between digital wallets, basic peer-to-peer transfer protocols, and actual savings hubs. Knowing the difference ensures you do not inadvertently stash thousands of dollars in an uninsured digital limbo.

P2P Networks and Wallets

People routinely assume payment gateways act exactly like a traditional branch. We see immense confusion primarily regarding three major household names:

- Zelle: This is a completely free P2P network built directly inside partner bank apps. Zelle is not a bank account, it holds zero balance of its own, and it pays zero APY.

- Apple Pay: This acts as a free contactless wallet bridge for your existing physical or virtual debit cards. It is not an actual localized checking product.

- GoHenry: This platform is a specialized kids and teen debit card system for the US and UK. You pay a monthly subscription for parental controls rather than viewing it as a primary yielding platform.

How Secure is Digital Banking?

Security is naturally the loudest reservation consumers state when ditching traditional, vault-centered branches. If you cannot walk in and demand your money from a teller, you must implicitly trust the app interface. The good news is that verified U.S. online platforms operate under identical federal regulations to neighborhood lenders.

Understanding the FDIC and Pass-Through Insurance

The backbone of American financial security is the Federal Deposit Insurance Corporation. Even if a digital bank does not retain its own direct charter, its partner institution provides security. The standard FDIC insurance limit fully covers depositors up to $250,000 per depositor, per insured bank, per ownership category.

Before opening any digital banking profile, locate the specific partner bank listed in the site footer. If your neobank suddenly enters liquidation, your underlying cash within that $250k limit remains entirely guaranteed by the federal government. Account protection works seamlessly regardless of app crashes or corporate bankruptcy.

App-Side Protections and Best Practices

Your actual daily risk stems less from bank failure and vastly more from credential theft. Neobanks build aggressive security tools directly into the core user interface. You manage your entire security posture from the settings tab.

We strongly recommend practicing strong account hygiene immediately upon origination. Enable multifactor authentication (MFA), utilize a completely unique password, and strictly adhere to device biometric locks. Configure real-time transaction alerts via push notification so you can instantly recognize and freeze your card if an unauthorized purchase hits.

Step-by-Step: Choosing Your Next Digital Banking Platform

Selecting a new provider should not feel like an overwhelming chore. Your strategy completely hinges on what exact features you value most on a daily basis. The process of migrating your daily financial life is entirely painless if mapped correctly.

Step 1: Analyze Your Cash Handling Flow

Identify exactly how you deposit and interact with your funds. Do you routinely receive physical cash tips from a service job? If you handle greenbacks daily, digital banking features require careful navigation.

Many digital platforms do not allow totally free cash loads, forcing you to pay a few dollars at a pharmacy register like Walgreens or CVS. However, platforms like Current offer 40,000+ fee-free Allpoint ATMs for simple access to withdrawals. Ensure the deposit pathways fit your work reality.

Step 2: Audit Current Bank Fees

Pull your last three monthly statements from your legacy traditional bank account. Look specifically for monthly maintenance fees, sneaky minimum-balance penalties, and out-of-network ATM hits. Traditional giants like Chase still mandate a monthly fee on their Total Checking product, though they do allow waivers via direct deposits.

Compare those cumulative losses against the totally free baseline of neobanks. We frequently discover readers are losing $150 to $200 a year purely on incidental maintenance friction. Eliminating that drag immediately compounds your annual saving outcomes.

Step 3: Match the APY Conditions

Never blindly trust a marketing headline flashing a high APY. Compare APY on the exact product tier you intend to use. Some platforms severely restrict where the high yield actually applies.

For instance, we love the Chime Prime tier offering 3.75% right now. But if your paycheck consistently falls under $3,000 monthly, you will permanently miss out on that specific condition. Choose a provider whose conditions effortlessly match your natural direct deposit cadence.

“Don’t chase a flashy 5.00% yield if the direct deposit hoops actively stress you out every single month. Real wealth building requires automated peace of mind.” – Ryan Cooper, Head of Content

Exploring Hybrid and Niche Account Types

Sometimes a straightforward high-yield pivot doesn’t cover hyper-specific consumer demands. The broader digital banking sector has fractured beautifully into niche use cases over the past three years. You can easily find tools dedicated specifically to building credit or protecting youthful spending behaviors.

Blended Checking Alternatives

Certain players merge checking dynamics seamlessly with auxiliary tools. Current, for instance, focuses highly on targeted lifestyle rebates alongside early direct deposit clearings. You can reliably achieve bonus “boosts” that elevate savings returns up to ~4.00% on strictly capped balances.

Similarly, PayPal holds immense weight in the digital space for freelancers. In 2026, real PayPal Savings exists within the US ecosystem. It is explicitly FDIC-insured via Synchrony Bank, offering genuine growth vectors without requiring users to offload funds into a disconnected app environment.

International Business Considerations

Digital banking transforms sole proprietors operating over borders. Traditional banks routinely delay international corporate wires for days, charging completely opaque spread margins while you wait. Modern commercial platforms bypass this old SWIFT system fatigue entirely.

If you bill clients globally, integrating with a platform like Monese continues to offer solid traction. Monese is still operating smoothly in 2026 across the UK and broader EU with multi-currency setups, remaining FSCS protected in the UK. Combining app-first UX with immediate localized routing codes fundamentally accelerates global invoice settlement.

The Realities of Migrating Your Direct Deposit

The most anxiety-inducing moment for new digital banking adopters involves shifting their primary paycheck away from an old account. They fear missing a rent cycle or triggering an overdraft during the swap. When testing Chime review procedures, we strictly analyzed their automated deposit routing tools.

Almost every high-tier neobank utilizes seamless payroll switching aggregators directly inside the app interface. You simply log in to your employer payroll system through the bank’s portal, and the routing numbers update automatically. It requires literally three taps on your screen to redirect tens of thousands of dollars.

We always advocate keeping your legacy branch account open and funded for exactly one full paycheck cycle. Wait until you witness the new digital banking platform successfully capture the incoming wire. Once that cash clears on the app, officially liquidate and close the old brick-and-mortar account.

Is Digital Banking Truly the Better Choice?

The data driving the market heavily points toward a permanent consumer shift. If you are deeply comfortable handling customer service tickets via chat interfaces and desire zero mandatory maintenance costs, the switch is a no-brainer. The high deposit yields completely overshadow legacy banking returns.

Traditional banks will undoubtedly survive because they service massive corporate debt, handle complex physical mortgages, and facilitate localized estate planning. They clearly win if you require face-to-face loan officers or handle massive daily amounts of retail cash. The Federal Reserve closely monitors how both sectors operate to preserve broad systemic stability.

Yet for the everyday consumer optimizing a standard paycheck, digital banking is overwhelmingly superior. By paying attention to exact FDIC guidelines, utilizing strict multifactor authentication, and aggressively evaluating the fine print on tiered APYs, you control your money on your exact terms. The era of settling for 0.01% yields is officially dead in 2026.