Written and reviewed per our independent editorial methodology.

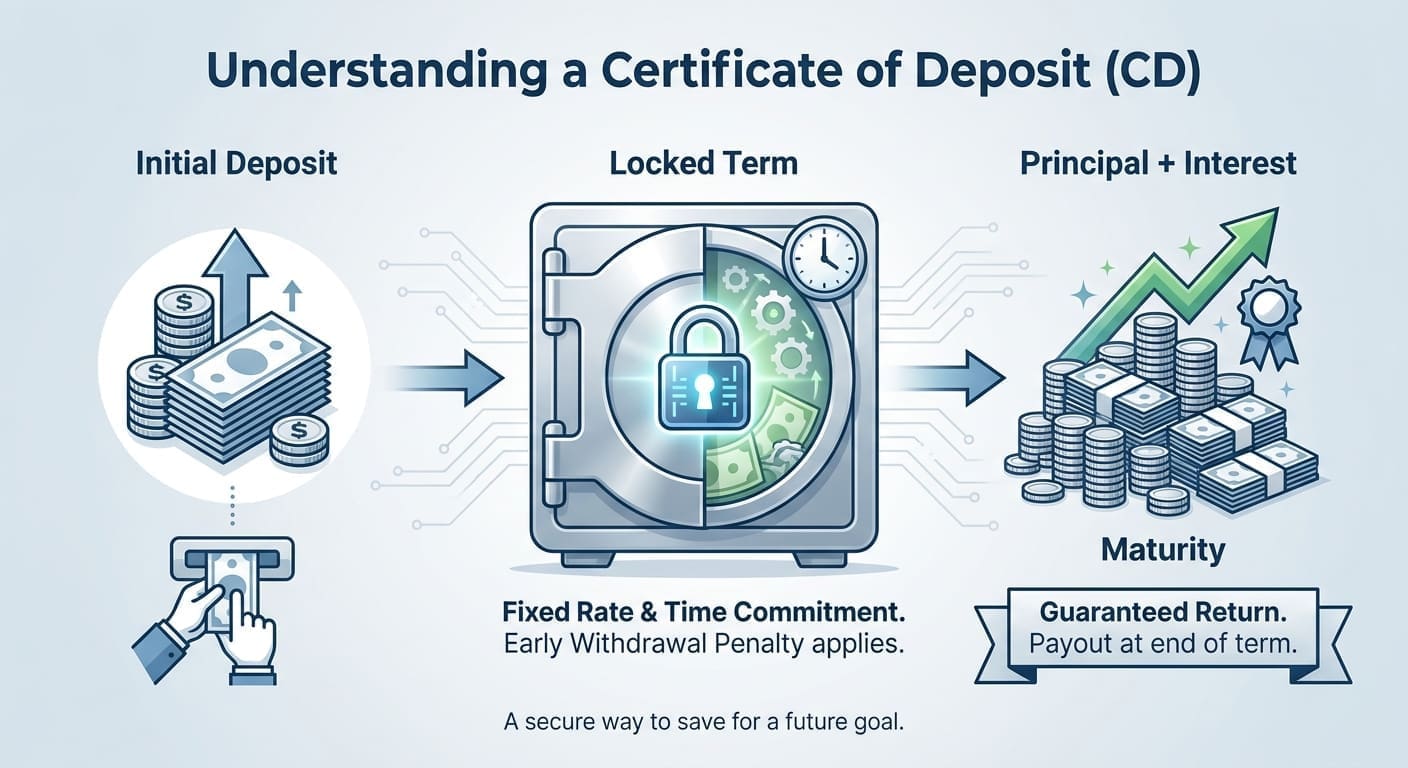

A Certificate of Deposit (CD) is a low-risk, FDIC-insured bank account where you deposit a lump sum for a fixed period to earn a guaranteed interest rate. In exchange for locking up your money until the maturity date, you receive a fixed Annual Percentage Yield (APY) that protects your returns from market drops.

If you are looking for a safe place to park your cash while earning a predictable return, you might be asking exactly what is a CD. A Certificate of Deposit is a foundational financial tool for conservative savers. It offers a fixed interest rate in exchange for a specific time commitment.

As a data-first analyst, I always look at the yield cap and the safety net before chasing flashy promotions. The math on a CD is incredibly straightforward and reliable. You lock in a rate today, and that exact rate stays with you until the term ends, regardless of market conditions.

There are no surprises, no sudden rate drops, and no market volatility to erode your principal. We are going to break down the exact mechanics of these accounts. By the end, you will know precisely how to leverage a CD to protect and grow your wealth.

- ✓CDs offer a fixed APY that cannot change during your chosen term length.

- ✓Your deposits are insured up to $250,000 by the FDIC or NCUA.

- ✓Withdrawing your money before the maturity date triggers a penalty, often costing months of interest.

- ✓Terms typically range from one month to five years, with longer terms generally offering higher yields.

The Core Definition: What Is a CD Exactly?

Let us start with the basics. A Certificate of Deposit is a specialized savings account offered by banks and credit unions.

You agree to leave a lump sum of money untouched for a specific period. This period is known in the banking world as the term length.

In return for your commitment, the bank pays you a fixed Annual Percentage Yield, or APY. This rate is typically higher than what you would get from a traditional savings account.

Here is the deal: The bank uses your locked funds to issue loans to other customers. They pay you a premium for providing that financial stability.

You cannot add more money to a standard CD once it is open. It is a strict one-time deposit.

When the term ends, the CD reaches maturity. You then get your original deposit back, plus all the accrued interest.

If you want to understand how this compares to other accounts, you might want to learn what a high yield savings account is.

How Does a Certificate of Deposit Work?

The mechanics of a CD are simple but rigid. You start by selecting a term length that fits your personal financial timeline.

Common terms range from three months to five years. Once you choose the duration, you make your initial minimum deposit.

Minimum deposits vary widely by institution. Traditional CDs often require $500 to $1,000 to open the account.

Jumbo CDs demand a much larger upfront commitment. These typically require at least $25,000 but sometimes offer slightly better rates for the volume.

The bank calculates your return using the APY. This metric includes the effect of compounding interest over a full calendar year.

Your interest usually compounds daily or monthly, depending on the specific bank. It is then credited to your account balance periodically.

The Critical Metric: APY vs Interest Rate

As an analyst, I see people confuse nominal interest rates with APY all the time. The distinction is absolutely vital for projecting your returns.

The nominal interest rate is simply the base percentage the bank pays on your money. It does not account for the power of compounding.

Listen closely: APY stands for Annual Percentage Yield. This is the real number that dictates your final payout.

APY factors in how often your interest is added to your balance. When interest earns its own interest, your money grows exponentially faster.

Always compare CDs using the APY. It provides a standardized, mathematically sound way to measure true earning potential across different banks.

If you are curious about the exact math, check out our guide on what is APY for a deeper dive.

A CD that compounds daily will yield slightly more over a year than one that compounds annually, even if the base interest rates are identical.

The Catch: Early Withdrawal Penalties Explained

The fixed rate of a CD comes with a strict condition. You must leave the money alone until the maturity date arrives.

If you pull your funds out early, the bank will hit you with an early withdrawal penalty. This is almost never a flat fee.

Penalties are usually calculated as a specific number of days or months of interest. The exact amount depends heavily on your term length.

For a one-year CD, you might lose 60 to 90 days of interest. For a five-year term, the penalty could easily be 150 days of interest or more.

Be warned: If you withdraw very early in the term, the penalty can eat into your principal deposit. You could walk away with less money than you started with.

This is exactly why CDs are terrible for emergency funds. You need highly liquid cash for emergencies, not locked-up capital.

- Penalties are usually calculated as days of interest earned.

- Short terms often carry penalties of 30 to 90 days of interest.

- Long terms can penalize you 150 days to a full year of interest.

- Severe penalties early in the term can actually reduce your original principal.

Are CDs Safe? The FDIC Insurance Net

Safety is the primary reason investors choose certificates of deposit. They are widely considered one of the lowest-risk investments available anywhere.

This safety is not just an empty promise from the bank. It is backed directly by the full faith and credit of the United States government.

Bank CDs are insured by the Federal Deposit Insurance Corporation. Credit union CDs are similarly insured by the National Credit Union Administration.

The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This is a hard, non-negotiable cap.

If you have more than $250,000, you must spread it across multiple banks to maintain full coverage. Never exceed the cap at a single institution.

You can verify a bank status directly on the official FDIC website. Always check this database before depositing large sums.

For more context on banking safety, you might ask is Chime safe to see how modern fintechs handle deposits.

No depositor has ever lost a penny of FDIC-insured funds since the FDIC was created in 1933.Federal Deposit Insurance Corporation (FDIC)

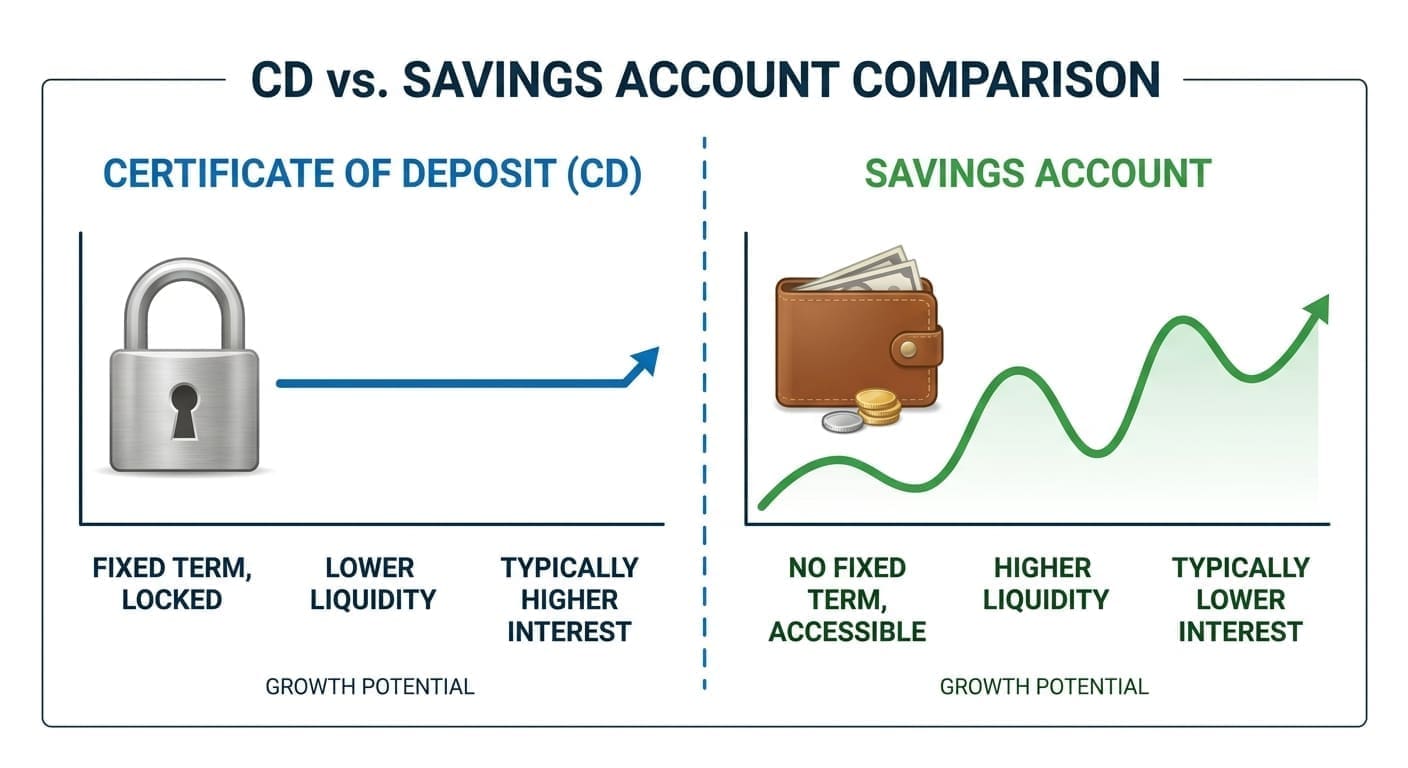

CD vs High-Yield Savings Account

The biggest debate for conservative savers is choosing between a CD and a high-yield savings account. Both options offer incredible safety.

A high-yield savings account provides liquidity. You can move money in and out relatively freely without facing harsh financial penalties.

However, savings account rates are variable. They can drop at any time if the Federal Reserve cuts benchmark interest rates.

A CD locks in your rate for the entire term. If market rates plummet tomorrow, your CD APY remains exactly the same.

The trade-off is simple: You sacrifice daily liquidity for absolute rate certainty. You have to decide which feature matters more for your specific goal.

If you are saving for a house down payment in exactly two years, a two-year CD is mathematically perfect.

You can see how different platforms compare in our SoFi vs Ally analysis.

How the Federal Reserve Impacts CD Rates

Banks do not pull CD rates out of thin air. They base their promotional offers heavily on the broader macroeconomic environment.

The most significant factor is the federal funds rate set by the Federal Reserve. This is the baseline rate banks charge each other for overnight lending.

When the Federal Reserve raises rates to combat inflation, banks raise their CD yields to attract more retail deposits.

Conversely, when the Fed cuts rates to stimulate a sluggish economy, new CD offers will drop very quickly.

Timing matters: If you lock in a long-term CD right before rates fall, you win. You get to keep the high yield while others suffer.

If you lock in right before rates rise, you miss out on better returns. This dynamic is why many investors use a strategy called a CD ladder.

Top CD Options to Consider Right Now

Finding the right CD means looking at the APY, the minimum deposit, and the penalty structure. Not all banks are created equal.

Online banks consistently offer higher rates than traditional brick-and-mortar branches. They have lower overhead costs and pass those savings directly to you.

You might want to read our digital vs traditional banks guide to understand this pricing dynamic.

Always read the fine print regarding what happens at maturity. Most banks will automatically renew your CD if you do not intervene.

You usually have a grace period of seven to ten days to withdraw your funds after maturity. Do not miss this critical window.

Let us look at a few strong contenders in the current market. These institutions offer competitive yields and highly transparent terms.

Frequently Asked Questions

Can I add money to a CD after I open it?

Generally, no. Traditional CDs require a single, lump-sum deposit at opening. If you want to invest more money later, you will need to open a new CD at the current market rate.

What happens when my CD reaches maturity?

You enter a grace period, usually lasting seven to ten days. During this time, you can withdraw your principal and interest without penalty. If you do nothing, the bank will often automatically renew the CD for the same term length at the new current rate.

Are CDs a good investment for beginners?

Yes, CDs are excellent for beginners seeking low risk. They provide a guaranteed return and are FDIC-insured up to $250,000, making them much safer than stocks or mutual funds.

How is a CD different from a regular savings account?

A savings account allows you to deposit and withdraw money freely, but the interest rate can change at any time. A CD locks your money in for a set period, but guarantees the interest rate will not change during that term.

Do I have to pay taxes on CD interest?

Yes. The interest you earn on a CD is considered taxable income by the IRS. Your bank will send you a 1099-INT form at the end of the year detailing the total interest earned.